Posted on Dec 9, 2024

Contemplating a fixed deposit to grow your money? Great! Now you have more reasons to invest in a fixed deposit besides that it offers safe returns. You can also get high interest rates. But still, there’s some due diligence to do. Even after choosing the best fixed deposit interest rate, you need to opt for the right interest compounding frequency to achieve your goal corpus. Besides, there are so many other things to consider. Let’s check out the top five aspects you should consider before opening a fixed deposit account.

High Fixed Deposit Interest Interest Rates

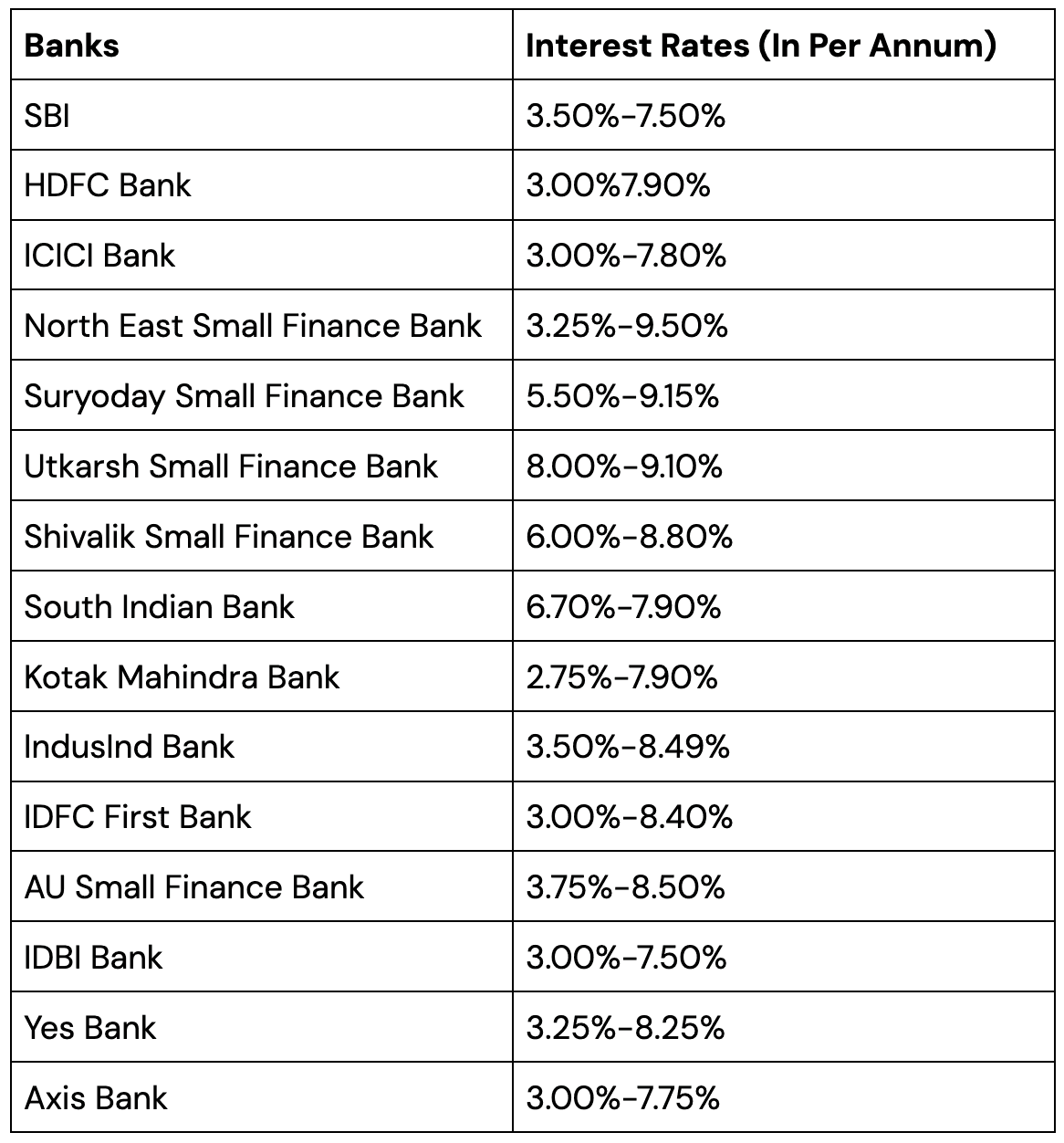

While shopping for a fixed deposit, your top consideration should be high interest rates. As of November 29, 2024, interest rates are as high as 9.30% per annum. As they can change periodically, stay updated with the rates when you are about to book a fixed deposit. Grab the offer at high interest rates to boost your savings.

Fixed Deposit Interest Rates of Top Banks for an Amount Less Than INR 3 Crore

Whether the Investment Amount & Tenure is in Sync with Your Financial Goals

What motivates you to invest is your financial goals. So, keep an eye on these while booking a fixed deposit. The goal corpus you set will dictate the investment amount and tenure you should go with. Here the FD calculator should come into play. The calculator will help you compute the maturity sum based on the investment amount, tenure and interest rate. Experiment with prevailing interest rates in the calculator to figure out the investment amount and tenure you should go with to achieve your goals.

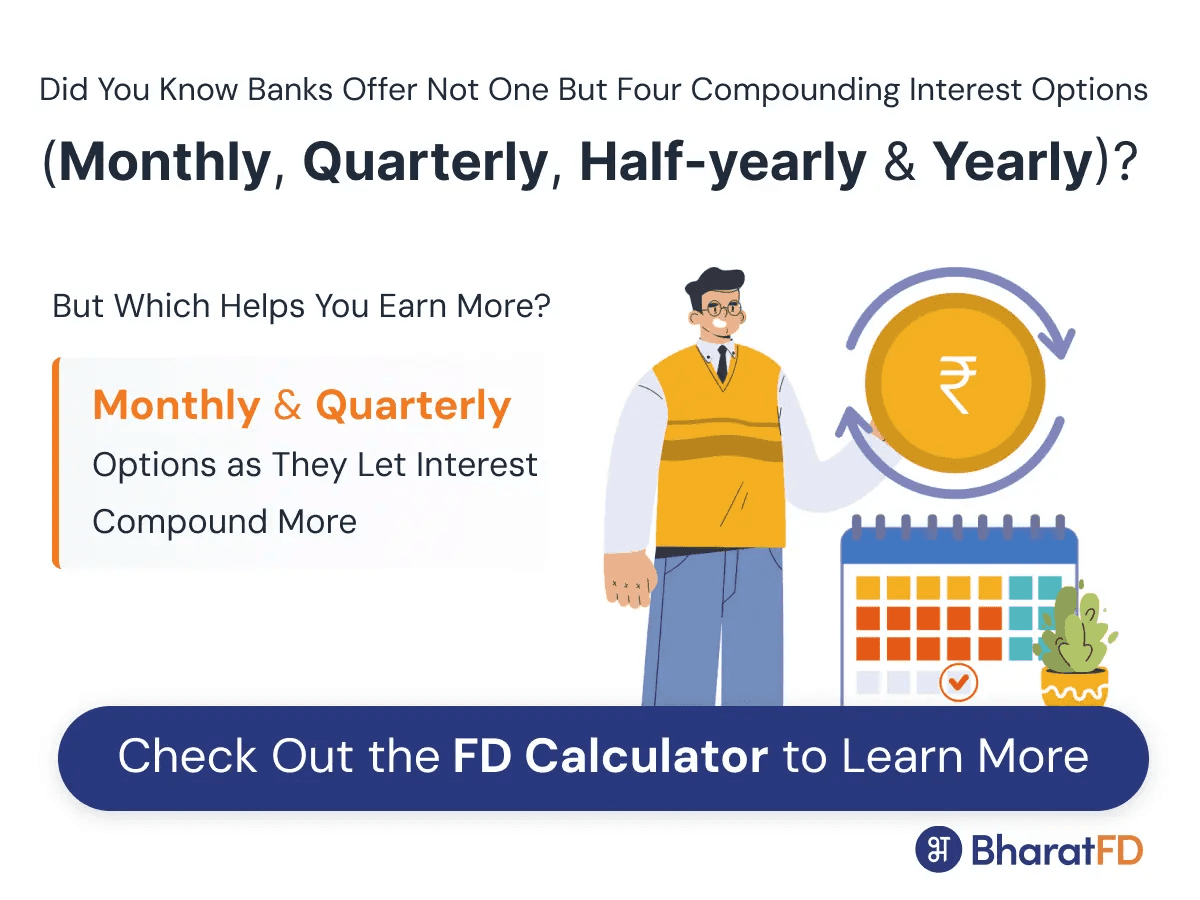

Consider Interest Compounding Frequency Options

While interest rates always remain the talking point, not many pay attention to the compounding frequency at which interest is calculated. Banks typically offer monthly, quarterly and yearly compounding interest options. Monthly and quarterly compounding interest options help raise your investments more than the annual compounding option.

Interest Payout Options - Should You Consider Choosing the Same?

Fixed deposits come with interest payout options too. The interest accrued on a fixed deposit will be paid to you monthly, quarterly or annually, depending on the payout frequency you choose. If you want regular income, consider choosing the interest payout option. However, if you want to raise your capital, choose the interest reinvestment option where interest is added to the principal amount based on the chosen compounding frequency.

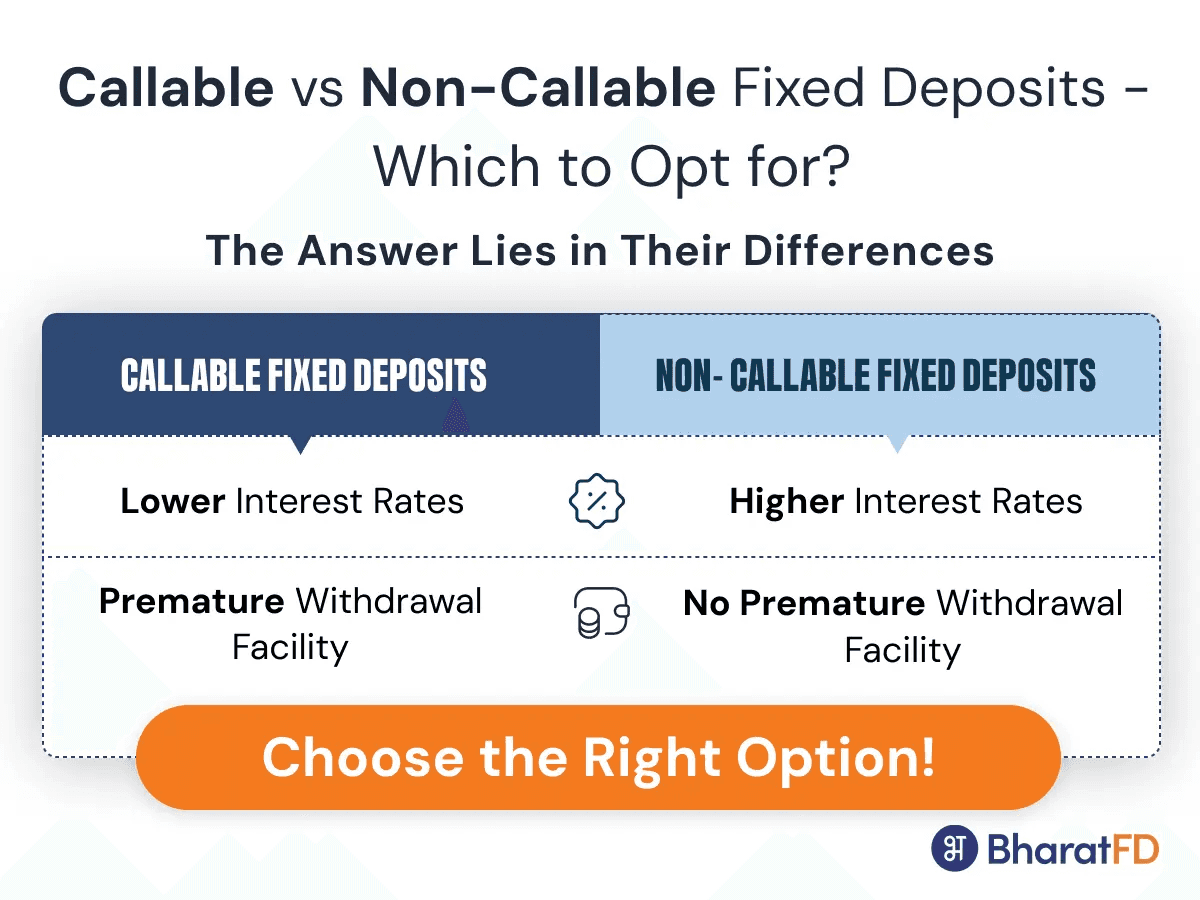

Callable vs Non-callable Fixed Deposits - Which Should You Opt for?

Banks offer both callable and non-callable fixed deposits. Non-callable fixed deposits come with higher interest rates compared to callable fixed deposits. Does that mean, should you prefer non-callable fixed deposits? Maybe not! Because these deposits don’t allow premature withdrawals. So, in case you face an emergency and you have to withdraw your savings, you cannot do so with a non-callable fixed deposit. However, callable fixed deposits offer you a premature withdrawal facility.

Conclusion

When choosing a fixed deposit, interest rates should not be the sole consideration. Check your maturity amount using the fixed deposit calculator online. Choosing the monthly compounding interest option is vital to creating maximum savings. In case you have a lump sum amount to invest but have an irregular flow of income, consider using the interest payout option of a fixed deposit. After all, it’s all about being flexible to meet your financial goals.