Posted on Dec 11, 2024

Vikas Chandra Das

Financial Content Expert & Brand Storyteller

Want to maximise your earnings with a financial instrument that offers safe returns regardless of market movement? You can’t take your eyes off fixed deposits that offer returns as per the booking rate. So, even if the market falls later, your returns will grow at the booking rate, a remarkable feature that stands out for many seeking safe investments in uncertain times. That’s why fixed deposits are increasingly becoming the choice of Indian families. As per the SEBI survey, as much as 95% of Indian families trust fixed deposits. While that speaks volumes for fixed deposits, there are ways to multiply your earnings through the same. One such way is implementing the fixed deposit laddering strategy.

You might wonder, how out of this world this laddering fixed deposit aspect comes out. Well, many are multiplying their wealth using this simple yet innovative wealth creation strategy. So, without any further delay, let’s discuss what it is, how it works, its advantages and several other details that matter.

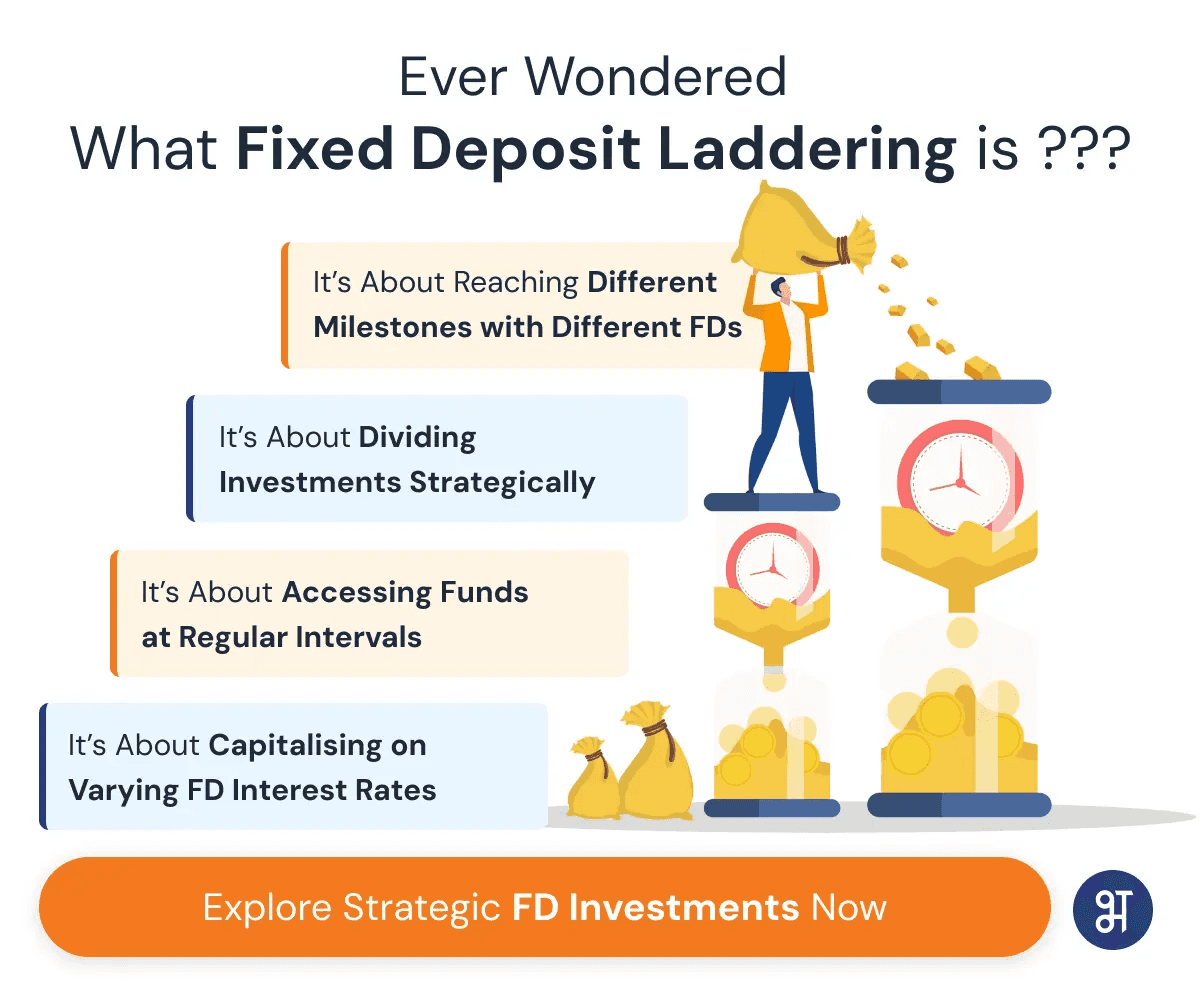

What is FD Laddering?

FD laddering is a more strategic approach to accomplishing your financial goals. It’s about dividing your lump sum savings into different fixed deposits with varying maturities of say a year, three years, 5 years, and so on. This staggered approach helps you capitalise on varying fixed deposit interest rates to increase earnings. The key here is to ensure safe returns and access to funds at regular intervals, helping you accomplish your several short and long-term financial goals.

Illustration Showing the Earnings from Implementing FD Laddering Strategies

You have a lump sum amount of INR 3 lakh to invest. You choose to invest it across different maturities - 2 years, 3 years and 5 years. So, you divide the sum into say INR 1 lakh each for these tenures. The interest rate remains 6%, 9% and 7% for 2, 3 and 5 years, respectively. So, how much will end up across each tenure? Let’s find out in the below table.

Note - The maturity sum is calculated based on monthly compounding frequency, which helps generate maximum earnings for fixed deposit investors.

Advantages of FD Laddering

Laddering fixed deposits has considerable advantages besides multiplying returns for the investors. Let’s check it out!

Higher Average Returns

What fixed deposit laddering does is that it allows you to reap gains from the interest rate differentials. You can thus opt for both short and long-term fixed deposits to meet your several financial goals along the way. The illustration above demonstrates higher average returns you can lock with fixed deposits of different tenures.

Higher Liquidity Adds to the Investment Appeal

Besides returns, what drives investors more is the scope for high liquidity. Financial emergencies can be the case with anyone. So, an investment with high liquidity is always welcome. However, the liquidity should not come at the expense of breaking your investments. You can avoid these by fixed deposit laddering. With this, there are high chances of FDs maturing when you need them instantly. You can use the proceeds of short-term FDs and let the long-term FDs continue to compound. It’s all about the balancing act that you need to do to perfection.

Allows You to Adjust to Interest Rate Fluctuations

Markets don’t remain the same throughout; there will be ups and downs affecting your investment value. However, there’s no effect of that on your fixed deposits as they yield returns at the booking rate. With fixed deposit laddering, you empower yourself more against market fluctuations.

For example, in today’s times when fixed deposit interest rates are as high as 9.50% per annum for three years, you can earn more with the laddering strategy. Consider booking different fixed deposits at different rates that prevail now. Tomorrow, if the market falls, you will continue to earn at higher rates compared to a small investment in one fixed deposit and holding back further investments.

Disadvantages of Fixed Deposit Laddering

Fixed deposit laddering has no disadvantages unless you decide to invest one now and hold back further for the future. Should the rates fall later, this delay will likely lower your earnings.

Strategies for Effective Fixed Deposit Laddering

Effective fixed deposit laddering comes with effective strategies aligned with your financial goals and risk appetite.

Choose FD Tenures Based on Your Financial Goals

Check the financial goals you want to achieve before implementing the right fixed deposit laddering strategy. Your financial goals will help you decide the different FD tenures for which you should invest. So, you can book an FD of say INR 1,00,000 to arrange the down payment for a car in say 3 years. At the same time, you can book another FD of the same value for 8 years to arrange the down payment for a home purchase. Depending on your financial goals, you can decide the right maturity for all your fixed deposits.

Leverage the Power of Fixed Deposit Calculators

BharatFD, your go-to platform to book high-return FDs, comes with a fixed deposit calculator that helps you decide on different tenures to maximise.

Choose Different Banks for Fixed Deposit Laddering

Choosing a mainstream bank for a fixed deposit is indeed good. However, consider providing your investment portfolio a competitive edge by leveraging higher returns provided by small finance banks. These banks offer returns of upto 9.50% per annum. Doing so can help you achieve your financial goals easily.

Check Out the Times When You Would Want Cash

You must have set financial goals and the time to achieve them. Depending on the time when you would want cash, you can choose different tenures when implementing the FD ladder strategy. So, if you want cash for a wedding in a couple of years from now, consider choosing an FD with a tenure of 2-3 years and another FD for 7-8 years to accomplish your other goals.

Make the Right Move Using the Interest Rate Trends

Keeping an eye on interest rate trends is pivotal to a successful wealth creation exercise. As of December 3, 2024, fixed deposit interest rates are going upward and the trend will continue for some time. So, maximise by locking different FDs for different tenures at relatively higher interest rates compared to when rates fall later.

Consider Opening Both Cumulative and Non-cumulative Fixed Deposits

Cumulative fixed deposits and non-cumulative fixed deposits are defined by their names themselves. While cumulative FDs reinvest the interest to help generate more earnings, non-cumulative FDs ensure interest payouts to investors at any of the monthly, quarterly, half-yearly or yearly intervals. While implementing the fixed laddering strategy, you can consider opening both cumulative and non-cumulative FDs for reinvestment and regular income purposes, respectively. That’s what you call aligning with two different requirements.

Consider Adding a Tax-saver FD to Bring Home More

Interest earnings from a fixed deposit are fully taxable. A 10% TDS is applied to fixed deposits with an interest income of more than INR 40,000 (Regular Customers) and INR 50,000 (Senior Citizens) in a financial year, respectively. So, along with regular fixed deposits, you can have a tax-saver fixed deposit too to save taxes. Yes, a 5-year lock-in period is imposed on tax-saver FDs. However, they offer tax deductions of upto INR 1.5 lakh in a financial year on the invested capital. This will help you bring home more. Like in a regular FD, here also, the tax applies to the interest income.

FD Terms & Conditions

Do read the fixed deposit terms and conditions while booking online. You can see the terms and conditions regarding the interest rate for each FD, premature withdrawals, etc. Being aware of these will help you avoid those last-minute surprises that usually remain the case for those who don’t pay attention to the terms and conditions.

Steps to Implement FD Laddering

Implementing the FD laddering strategy successfully requires being meticulous at each stage of the process. This is how you should approach it.

Determine the Amount You Should Look to Invest in FDs

This will depend purely on your financial goals. Calculations made based on the fixed deposit calculator will further decide the amount you should look to invest in FDs. So, you are planning to buy a car worth INR 5 lakh in 2 years. But as of now, you only have INR 1.50 lakh as of now.

Considering the prevailing FD rate of around 6% for 2 years, the maximum you can generate is INR 1,69,074, which is way short of the purchase amount. However, you can easily make the down payment, constituting around 10-20% of the car’s price. The down payment will come around INR 50,000-1,00,000. The rest you can arrange with a car loan.

You can thus make it bigger by investing INR 1.50 lakh in two FDs. Ideally, you should lock one FD of INR 90,000 for 2 years and another INR 60,000 for five years. With this arrangement, you will receive INR 1,01,444 from an FD of INR 90,000 for 2 years at 6% per annum. Whereas the INR 60,000 investment for five years will help you accumulate INR 87,198 at 7.5% per annum.

Choose Different FD Tenures

Choosing different fixed deposit tenures correctly is crucial to fulfilling your various goals. In fact, the premise of the laddering strategy depends heavily on tenures. Tenures decide the interest rates to a great extent. The rates remain the highest in a 3-year tenure for most banks. With more time, the rates remain lower. However, as you give your investments more time with a longer tenure, you earn a substantial amount even then. Choose a 2-3 year fixed deposit to meet your short-term goals and a 5-10 year deposit to accomplish your medium and long-term goals.

Divide Your Investments Strategically

It pays to divide your investments strategically to meet your financial goals at different points of time. Short-term goals such as a bike or car purchase can be achieved with slightly smaller investments compared to long-term goals such as a home purchase.

Wrapping Up

Fixed deposit laddering is an effective strategy to ensure higher average returns, reduce liquidity risks and prevent incidences of penalties on premature withdrawals. Using the FD calculator on Bharat FD, your go-to platform to book high-return fixed deposits, is one practical way to ensure the same.

FAQs

How can I get the maximum return from a fixed deposit?

Use FD laddering to optimise returns by investing in fixed deposits with varying tenures.

Can I invest in FD multiple times?

Yes, you can do so by exploring FD laddering by which you can open multiple FDs with different maturity periods.

Are FDs better than stocks?

FDs are safer but offer lower returns than stocks, which, on the other hand, are riskier but can generate higher returns.

How should I distribute the maturity periods in an FD Laddering Strategy?

Distribute across a range of maturities to access funds periodically and benefit from higher interest rates.

How do interest rate variations affect my FD Laddering Strategy?

Interest rate variations will not affect your wealth creation exercise using the FD laddering strategy if you invest in different FDs at a time when interest rates are generally high. However, if you invest in one FD now and invest further at a time when rates are lower, you miss out on the opportunity to maximise.

Reference