Posted on Dec 20, 2024

Vikas Chandra Das

Financial Content Expert & Brand Storyteller

The tale of Ravi and Shankar with fixed deposits is something to read and learn from. Both used to work in a software company and one day, they thought of opening a fixed deposit account. A few days later, both Ravi and Shankar opened an FD for eight years. While Ravi went through every detail surrounding a fixed deposit, Shankar was content with grabbing high interest rates alone. Interestingly, a couple of years later, both went jobless and required instant cash to meet their emergency needs.

While Ravi was able to withdraw, Shankar could not. What?? Yes, but true! Ravi kept money in a callable fixed deposit that allows premature FD withdrawal, Shankar put it in a non-callable fixed deposit that disallows the same. Because Shankar was concentrating only on high interest rates offered on a non-callable FD, he could not factor in the potential emergency needs and had a not-so-good experience later.

What is the Premature Withdrawal of FDs?

FD premature withdrawals refer to taking out money from a fixed deposit before it matures. So, if you have opened a fixed deposit account for 10 years and want to withdraw funds from it after 5 years due to an emergency, you can do so using the premature withdrawal facility. However, do check for this facility while opening an account so that you don’t have to face what Shankar had to. Situations that warrant premature withdrawal include cash needs due to incidences such as weddings, jobless situations or any other emergency.

There’s a Catch with Premature Withdrawal - The Penalties

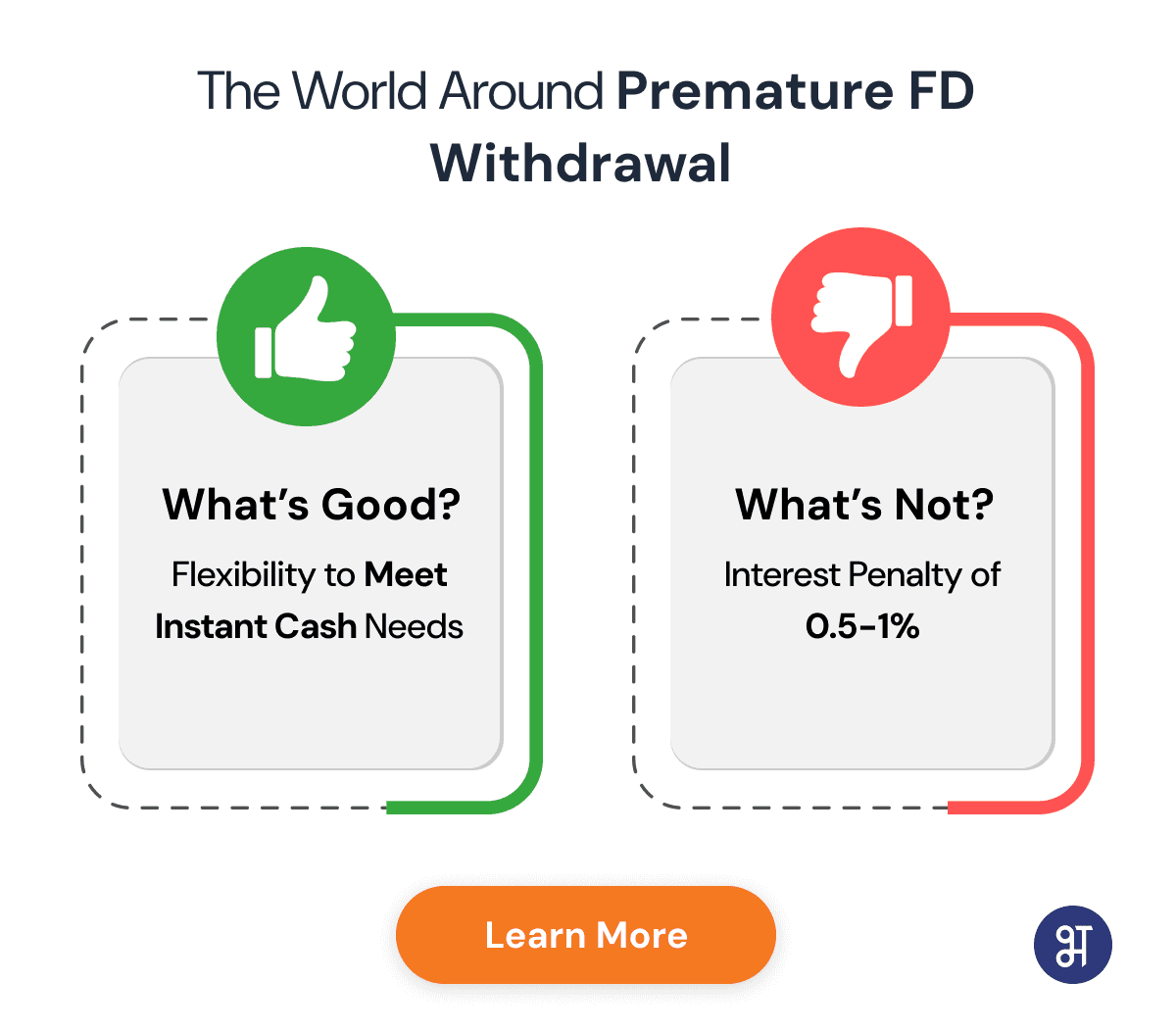

Premature FD withdrawals offer you the required flexibility should you face emergencies. However, banks debit penalties of 0.5-1% of the withdrawal amount. The reduction in return is obvious with this. But how much will it be? Let’s calculate and find out!

Example - You invest INR 5 lakh for 5 years at 7.50% per annum. After three years, you find an emergency and want to withdraw. In three years, your FD value will touch INR 6,24,858. Suppose the bank levies a penalty of 0.50% for premature withdrawal. In that case, the penalty amount will be INR 3,124.29. You will get INR 6,21,730.71.

The bank will also deduct TDS on the interest earned upon withdrawal. You will likely earn interest worth INR 44,747. Since it has gone past the threshold limit of INR 40,000, the bank will deduct TDS at 10% on INR 44,747. The TDS amount will thus be INR 4,474.70. This amount will also be deducted. So eventually, you will have INR 6,17,256.01.

Note - FD interest calculations are made on a quarterly compounding basis.

Disadvantages of Premature FD Withdrawal

FD withdrawal before maturity comes with its share of pitfalls. Let’s learn about them.

Loss of Interest Income

Premature withdrawal from a fixed deposit leads to the loss of interest earnings for investors. The loss comes as an interest penalty on the withdrawal amount. So, keep this in mind when withdrawing.

Impact on Your Financial Goals

You invest in a fixed deposit to achieve certain financial goals, right? If you open a fixed deposit of INR 8 lakh at 7.50% per annum, you will accumulate INR 11,59,959 at the end of five years. In case you want to withdraw before three years, the accumulated proceeds at that time will be INR 9,99,774. This amount will further see the 0.5% premature withdrawal penalty of INR 4,998.87 and 10% TDS i.e. INR 7,711.80. Factoring in the same, your eventual amount will reduce to INR 9,87,063.33. So, see whether the reduced amount is sufficient for your financial goals.

Opportunity Costs

Premature FD withdrawals prevent you from maximising. So, there’s a loss of opportunity that can otherwise be tapped into by continuing your fixed deposit till its maturity.

Tips to Avoid Penalties on Premature Withdrawal

Penalties on premature withdrawal somewhat reduce your earnings. So, here we have listed out methods that can help prevent premature withdrawal instances and the penalties that follow.

Implement FD Laddering Strategy

It’s never a good feeling when you get less than what’s promised! With a fixed deposit laddering strategy, you will likely avoid premature withdrawals. The strategy revolves around splitting your lump sum savings into multiple investments for different tenures. This will ensure you have cash when needed without having to break a fixed deposit before maturity.

Loan Against Fixed Deposit

Sometimes the emergency may not be to an extent where you will need to withdraw the entire amount. If that’s the case, you can take a loan against a fixed deposit. This will ensure no breakage of a fixed deposit and let it earn the interest you always wanted.

Using Contingency Funds

If you have created a contingency fund, you can liquidate it to meet your instant cash needs without having to break your fixed deposit.

How to Close an FD Prematurely?

You can close an FD before its maturity date either at the bank branch or online. However, the online option would be better as you don’t have to move out of your home to do so. It takes just a few minutes. That being said, certain banks may not allow you to close a fixed deposit before maturity. In that case, you will need to visit the bank branch to do it. So why do the hustle when you can book an FD and close it whenever you want with a few clicks online? It’s a fixed deposit marketplace where you can see attractive offers from RBI-regulated banks. So, stay relaxed and enjoy the convenience, comfort and flexibility of BharatFD.

Summing Up

The premature withdrawal facility does offer you flexibility should you face cash emergencies during the tenure of a fixed deposit. However, the penalty of premature closure of FD will reduce your returns. So, it’s advised to factor in both short and long-term goals while going ahead with a fixed deposit. Opening multiple FDs with short and long tenures will ensure you achieve all your financial goals and potentially prevent incidences such as premature withdrawal and its penalties.