Posted on Dec 13, 2024

Vikas Chandra Das

Financial Content Expert & Brand Storyteller

Life is all about choosing the right companion at different stages to overcome different challenges that may arise. Companions don’t necessarily mean humans only, they can even be investments such as fixed deposits that are as safe as houses. The assurance fixed deposits bring to investors regardless of market ups and downs makes them feel confident about their future. And when safety comes with high returns, the joy doubles!

But then, there are many fixed deposit plans from which you need to finalise the one that serves your needs. Seems arduous! But we at BharatFD will help you select the right fixed deposit scheme through this guide. Take a look!

It All Starts with Understanding Your Investment Goals

Whatever financial instruments you choose to invest in, see how sync they are with your investment goals. As an investor, we can have short, medium and long-term goals, which we would like to achieve in 1-2, 3-5 and over 5 years, respectively. Fixed deposits are the right choice to achieve all these goals. Just choose the tenure as per your goals, and you are home!

For example, if you are eyeing short-term goals like an iPhone purchase, booking a fixed deposit plan for 1-2 years is advised.

If you want to accumulate the down payment for a car purchase, consider investing in an FD for 3-5 years.

Achieving long-term goals such as a home purchase will require investing for the long term in fixed deposits and other instruments.

Don’t Forget to Compare Interest Rates of Banks

When shopping for a fixed deposit, compare the interest rates of banks and non-banking financial companies (NBFCs) for different tenures. You should pick the one that offers you the highest interest rate for the time you are looking to invest in. For example, if you’re investing for 3 years, find a bank that offers the maximum for that period and lock the deal with it. You’ll be in surplus! BharatFD is your gateway to lock the high-yield FD deal by allowing you to compare and choose from an extensive list of RBI-regulated banks.

NBFCs - Should I Consider Opening a Fixed Deposit Account There?

Non-banking financial companies (NBFCs) offer higher interest rates compared to banks. But as an investor, you also need to check their credit ratings. Prefer an NBFC with a solid credit rating of AAA, AA instead of B, C and D. It’s all about being safe while enjoying high returns - the premise of a solid fixed deposit plan.

Interest Compounding Frequency - How Bigger a Factor is This?

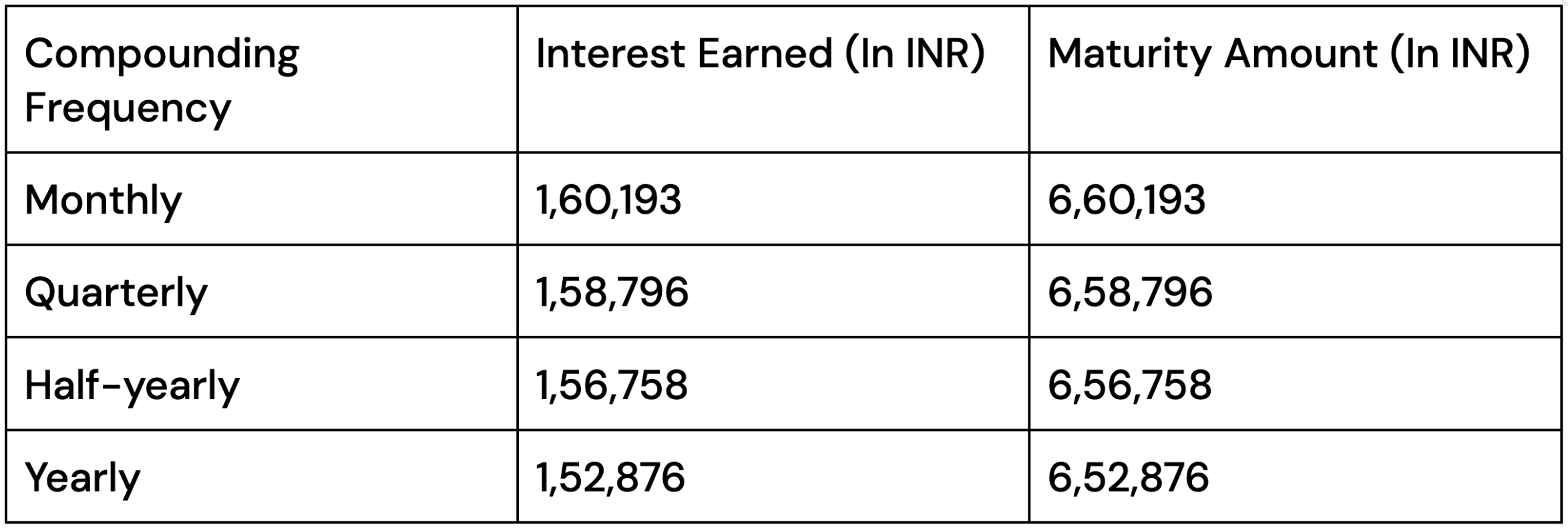

Locking the fixed deposit deal at high interest rates is the first step. The next step is to choose the right compounding frequency that will earn you the maximum on your investments. Banks typically offer - Monthly, Quarterly, Half-yearly and Yearly compounding frequencies. As the interest compounds more in monthly and quarterly options, people locking FDs with these stand to benefit the most. Let’s consider an example to understand the same.

Example - You want to book a fixed deposit of INR 5 lakh for 3 years at 9.30% per annum. Let’s check out the earnings from each of the interest-compounding frequency options.

Consider Liquidity Needs

Financial emergencies can strike anytime. Keeping in mind the same, consider choosing a fixed deposit plan that allows withdrawal before maturity. Also, look at the penalty for exercising this option. Usually, banks debit a penalty of 0.5-1% of your proceeds at the time of premature withdrawal. At the same time, look how much a loan you can avail of against a fixed deposit. Banks typically offer a loan at upto 80-90% of a fixed deposit. The best part is that you don’t need a credit history to access this loan.

Look for Different FD Options

It’s always a good idea to have options. Something you as an FD investor, you should always look for. As emerging needs can arise with time, being flexible by tapping into multiple options using the fixed deposit laddering strategy. Some popular options include cumulative and non-cumulative fixed deposit plans. While cumulative options enhance your returns by reinvesting interest at the chosen compounding frequency, non-cumulative options give you interest payouts to meet your regular income purpose. As a financial advisor, we recommend splitting your lump sum savings into these fixed deposit options. Choose the cumulative fixed deposit for the long term and non-cumulative for the short term.

Look for a Hassle-free Fixed Deposit Application

Find banks that allow you to open a fixed deposit easily. Some banks allow you to open a fixed deposit online, while others want you to visit a branch for the same. Looking at everyone’s hectic schedule, visiting a branch for a fixed deposit can be off-putting for many. Why not use BharatFD’s platform where banks with their attractive fixed deposit interest rates are there? No hassle of visiting the bank branch, no need for an existing banking relationship. It’s all smooth and synchronised at BharatFD. Try out!

Don’t Ignore Auto-Renewal and Flexible Tenure Options

If the fixed deposit you put your hand on comes with auto-renewal and flexible tenure options, your happiness will only multiply! With auto renewal, your fixed deposit proceeds will be automatically renewed for the same tenure. However, the interest rate for the same will be the one that prevails at that time. Fixed deposits come with flexible tenures ranging from 7 days to 10 years. There can also be tenures like 440 days or 765 days, for instance. So, you can imagine the flexibility you will have with such a fixed deposit plan.

Wrapping Up

The answer to - How to choose the right fixed deposit plan - lies broadly in your investment goal and the time for which you wish to stay invested. Maximising gains will require splitting savings into multiple high-yield FDs for different tenures. That will most likely prevent premature withdrawals and the penalty that follows. So, be aware, be choosy and be happy!