Posted on Dec 20, 2024

What type of investor are you? Does the rise and fall of the market and its effects on your investments affect you or do you stay unaffected? The answers to these questions determine the financial instrument - fixed deposit vs mutual fund - you will like investing in for wealth creation.

This assumes significance as people often commit mistakes when selecting between the two and put their finances at stake. We at BharatFD don’t want you to be in that situation! We thus make sure to put unbiased information surrounding fixed deposits and mutual funds so that you can achieve your goals without any hassles.

Fixed Deposits - An All-season Ally for Conservative Investors

Do you like stability when it comes to investments? Fixed deposits are the ones you should go with. It’s a product where you put a specific amount for a specific period at the prevailing interest rate.

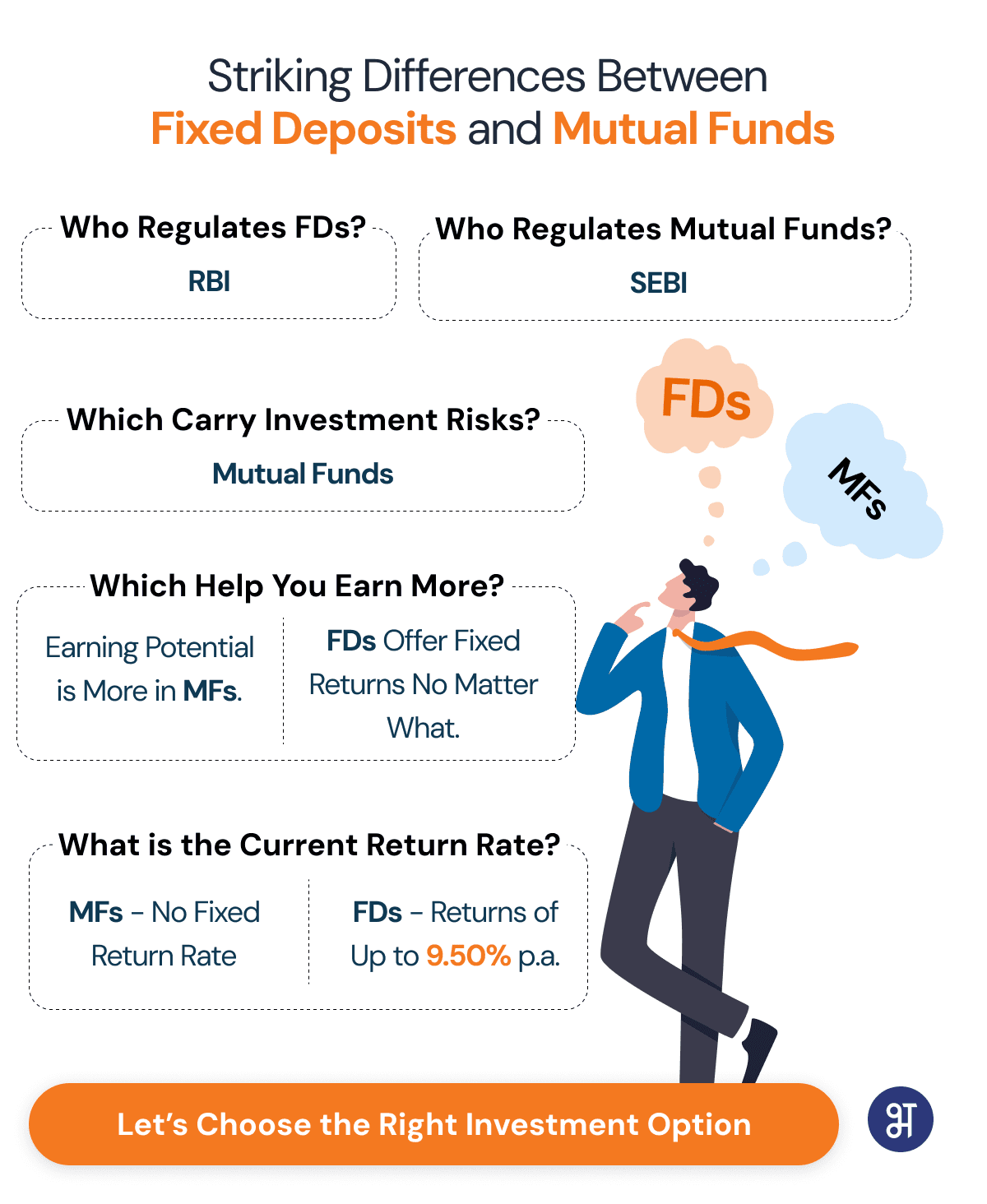

But choosing the right fixed deposit that compounds your wealth with an interest of upto 9.30% per annum, which prevails now, is equally important. With no market-linked risks, fixed deposits are your gateway to creating wealth without fear. So, if you book an FD at 9.30% per annum for five years, you will earn at that rate. Even if the fixed deposit interest rate in say 2 years drops to 8%, your 9.30% interest rate will remain intact.

Mutual Funds - An Investment That Interests Investors with Varied Risk Appetite

Mutual funds are an investment where the money you put in goes into a wide range of financial instruments depending on their types. These are broadly classified into equity, debt and hybrid mutual funds.

Equity mutual funds suit people with a flair for high investment risks in exchange for higher returns. So, how do they raise your money? They invest in a wide range of stocks aligned with your capital appreciation objectives.

What about debt mutual funds? How do they work and which type of investors will find great investing here? Debt mutual funds are a type of investment where the money goes into a wide range of bonds, debentures, certificates of deposit, commercial papers, etc. All of these come with a yield, subject to market risks, but not to the extent of equity. So, returns here are reasonably safe. It is therefore in direct competition with a fixed deposit. While fixed deposits deliver you returns promised while booking, debt mutual funds come with interest rate risks, maybe not on an elevated level.

Hybrid mutual funds invest in a combination of equity and debt instruments. So, investing here is like enjoying the benefits of two worlds - Capital Appreciation & Investment Safety. The extent of distribution in equity and debt instruments will depend on the type of hybrid fund you choose - Equity-oriented and Debt-oriented Hybrid Funds. Equity-oriented funds invest a minimum of 65% in equity and equity-related instruments. Similarly, debt-oriented funds put a minimum of 65% in debt instruments.

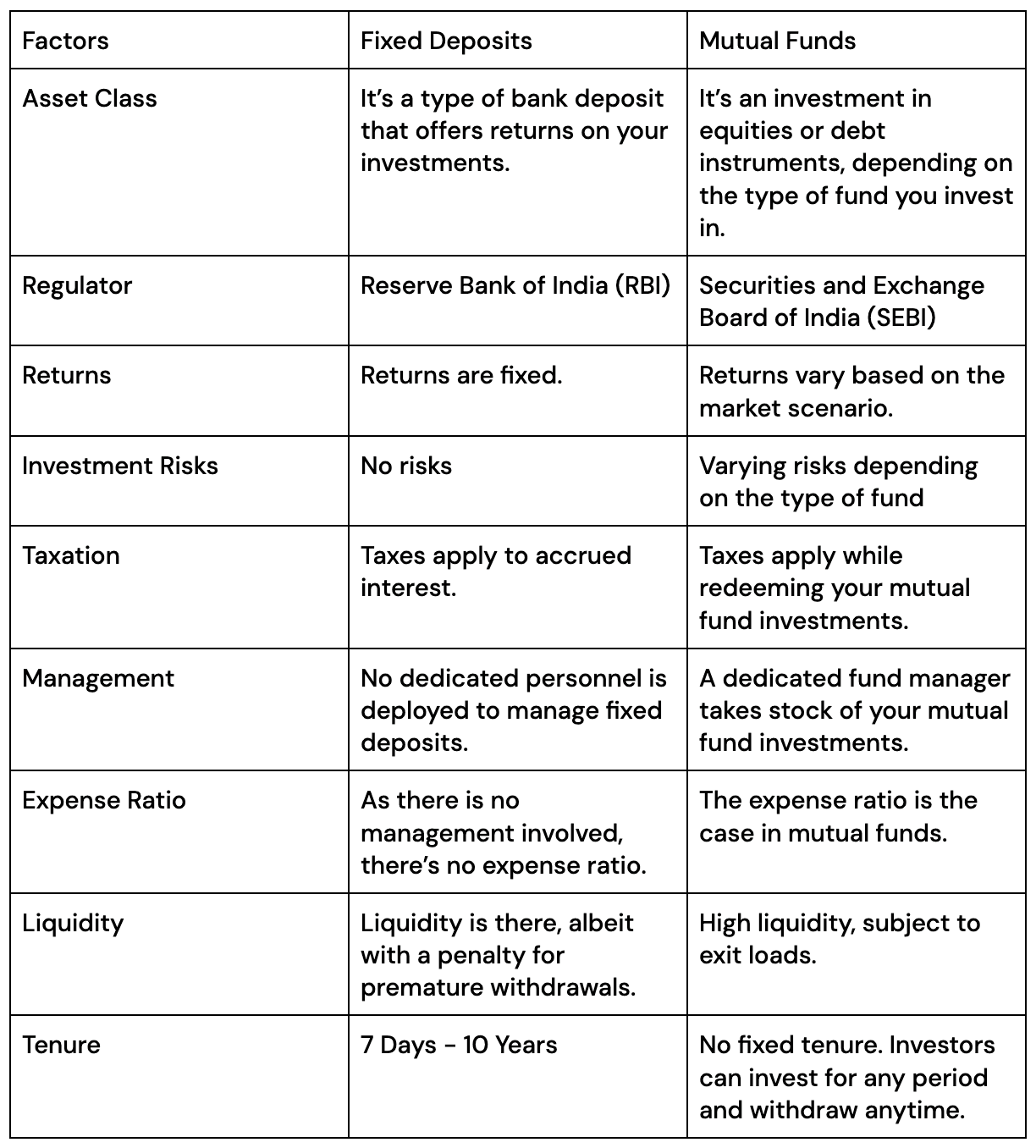

The Key Difference Between FD and Mutual Funds

Asset Class

In a fixed deposit, you invest a specific amount for a specific period. The money invested bears a specified interest rate. So, when the fixed deposit matures, banks pay the invested amount along with interest to depositors.

The asset class for mutual funds varies based on their types.

Equity Mutual Funds - Stocks & Other Equity Instruments

Debt Mutual Funds - Debt Instruments

Hybrid Mutual Funds - Equity/Debt Instruments

Regulator

Fixed deposits are regulated by the RBI. The regulator forms rules for banks offering fixed deposits to investors while staying vigilant to ensure no foul play.

For mutual funds, the SEBI stipulates rules for investments, exits, and much more. It is formed to protect the interests of investors while ensuring transparency in mutual fund transactions by enforcing existing rules and making amendments wherever necessary.

Returns

Fixed deposits come with fixed returns no matter what. The interest rate at which you book an FD will remain intact even if the rate during the investment journey falls. Simply put, the booking rate is your eventual return rate on a fixed deposit.

Mutual fund returns, on the other hand, are impacted by the market’s ups and downs. The return on an equity fund is affected by the performance of stocks it may have invested in. The greater the performance of the underlying stocks in the portfolio, the greater the return your investments will make and vice versa.

Similarly, the return on a debt fund depends on the performance of bonds, debentures and other debt instruments in the portfolio. In a nutshell, the mutual fund return rate varies based on the market movement. The return of a hybrid fund depends on its orientation. Equity-oriented funds will likely have greater returns than debt-oriented hybrid funds.

Investment Risks

The investment risks are not there for fixed deposit investors. All they need to do is select the fixed deposit for the period that can earn them at a greater interest rate.

Mutual fund investments, on the other hand, are subject to investment risks - the line you must have heard so many times watching ads on television and digital platforms.

Taxation

Taxes apply to fixed deposit investors when the interest accrued exceeds INR 40,000 for the general public in a financial year. Senior citizens will need to pay taxes when the interest accrued surpasses INR 50,000 in a financial year.

Management

Fixed deposits do not require any fund management on the part of the bank where you park your money. Whereas in mutual funds, fund managers keep mobilising your money from one financial instrument to another so that you can gain handsome returns.

Expense Ratio

As fixed deposits don’t involve fund management, there’s no expense ratio. So, as an investor, you don’t get any deductions from your gross earnings. However, the TDS will be debited as per the Income Tax laws. Whereas in a mutual fund, there’s an expense ratio involving the registrar, fund management and marketing fees, alongside other costs. These costs are debited from the Net Asset Value (NAV) of a mutual fund daily. Equity mutual funds will likely have a greater expense ratio than debt funds.

Liquidity

You can withdraw from fixed deposits before maturity. There will be a 0.5-1% penalty on your earnings till that time. You need to bear that as an investor. However, if you invest in a tax-saver fixed deposit, you can withdraw only after five years.

Mutual funds, on the other hand, will allow you to withdraw anytime. Here also, you will need to pay exit loads if applicable. Some mutual funds may not have exit loads. Here also, the capital gain tax will also apply. There are short and long-term capital gain taxes for both equity and debt mutual funds. Here’s a catch too! The definition of short and long-term capital gains for debt and equity funds varies from each other. Check out the table below to know the difference as well as the taxes that apply.

Tenure

Fixed deposits come with a specified tenure ranging from 7 days to 10 years. Money held for a minimum of seven days will yield interest at the prevailing rate. Whereas mutual funds don’t come with a specified tenure.

Benefits of Fixed Deposits

Steady Returns

The best part about fixed deposits is that they earn you steady returns regardless of what’s going on in the market. Your booking rate is your eventual rate provided you don’t withdraw before maturity.

Capital Preservation

The amount you invest in a fixed deposit along with the returns are safe from market fluctuations. No worries on that front! Knowing the same will only make you more confident about creating wealth through a high-yield fixed deposit.

No Investment Risks

With no market-linked risks, fixed deposits remain a beacon of hope and inspiration for conservative investors. These investors don’t like the thrill of market ups and downs affecting their investment value.

Tax Benefits

Regular fixed deposits don’t come with tax benefits. However, there are tax-saver fixed deposits you can choose to invest in to save taxes. Investments in tax-saver FDs allow you to gain tax deductions of upto INR 1.5 lakh in a financial year.

Liquidity

There’s always a possibility of you breaking your fixed deposits at the advent of any emergency that may arise. Banks allow you to break FDs. However, there’s a thing called fixed deposit laddering that potentially eliminates premature withdrawals and the penalty associated with the same. With laddering, you can open multiple fixed deposits with short and long tenures. So by the time you face an emergency, you will likely see an FD maturing, preventing you from breaking your investments.

Ease of Investment

Fixed deposits are easy to open. Compare and choose the fixed deposit of the bank you find is aligned with your financial goals.

Benefits of Mutual Funds

Diversification

What stands out for mutual funds is the diversification they bring to your investment portfolio. The money you invest here goes into various financial instruments such as stocks, bonds, debentures, etc. Going this way helps offset the effect of the fall in the value of one instrument with the rise in others. Investing in mutual funds reduces the risk compared to investing directly in financial instruments such as stocks, bonds and debentures.

Professional Management

Mutual funds are managed professionally by fund managers who use their market expertise to pick and choose financial instruments for wealth creation.

Liquidity

Mutual funds allow enhanced liquidity by allowing investors to withdraw anytime. So, if any financial emergency arises, you can withdraw money from your mutual fund to overcome the same.

Access to Asset Classes

Mutual funds invest in a wide range of asset classes such as equities, bonds, debentures, money-market instruments, etc. While equity funds invest predominantly in equities, debt funds put your money in bonds, debentures and money-market instruments.

Convenience

You can buy mutual funds easily online as well as check the statement to have an idea of where your investments stand.

Profit Potential

The return potential of equity mutual funds is massive as there’s no defined limit. Depending on how your investments fare, the returns will be calculated. A great run will see a monumental rise in returns, while a sluggish run will see returns growing at a slow pace. It’s completely dependent on the market. Debt funds, on the other hand, come at a lower return in exchange for lower risks.

How to Choose Between an FD vs Mutual Fund?

Choosing between a fixed deposit and a mutual fund depends on understanding your risk appetite and financial goals. If your risk appetite is high and you want to achieve a big corpus over say 10-15 years, investing in equity mutual funds will make sense. However, if you can’t stay calm while the market goes crazy with ups and downs, stay invested in a fixed deposit. You’ll appreciate the stable return on the investment.

Final Words

There are advantages and limitations with both fixed deposits and mutual funds. It’s about evaluating them carefully and choosing between an FD vs mutual fund based on your financial goals and risk tolerance. We at BharatFD will come with another story, another insight and another perspective. Till then, it’s goodbye!