Posted on Feb 20, 2025

FD vs Debt Fund - Where Should You Invest in to Meet Your Financial Goals?

A great investment life begins with a great investment choice you make from the available options. The selection becomes tricky when it’s about ensuring the safety of your hard-earned money. The two prominent options that come across for investors with a conservative mindset are fixed deposits and debt mutual funds. Both are similar yet come with a unique value proposition for investors. So, it makes sense to compare FD vs Debt Fund and find the right option based on your financial goals, risk appetite and investment horizon. So, what are you waiting for? Let’s start comparing!

Understanding Fixed Deposits and Debt Mutual Funds

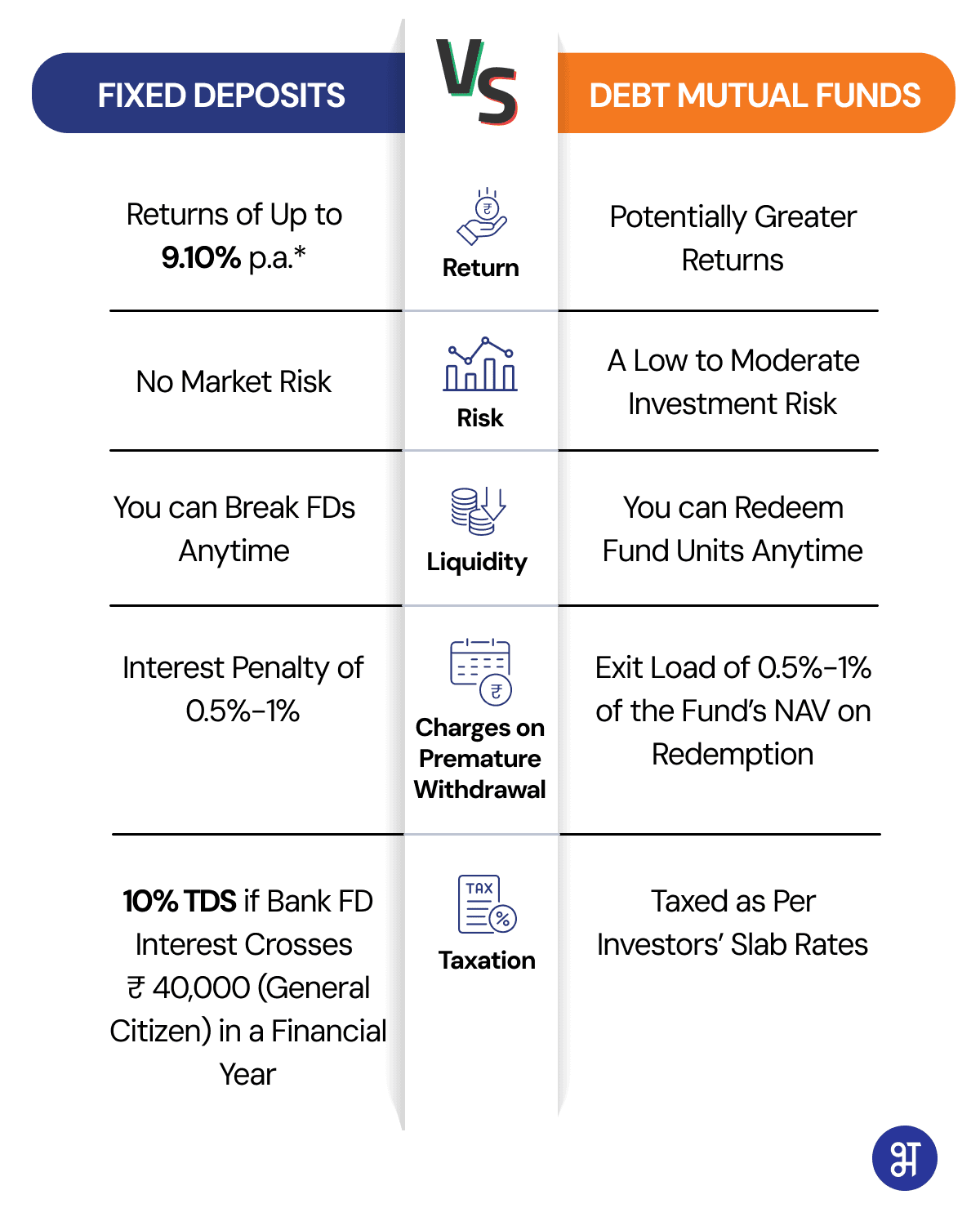

Let’s start with fixed deposits. These offer fixed returns to investors no matter what. Presently, fixed deposit interest rates are as high as 9.10% per annum. Investments start with an amount as low as INR 1,000. You can invest in it for a minimum and maximum tenure of 7 days and 10 years, respectively. Bank fixed deposits are backed by an insurance cover of up to INR 5 lakh by the Deposit Insurance and Credit Guarantee Corporation of India (DICGC). Just in case you want to withdraw funds before the maturity, you can do so using the premature withdrawal facility.

In contrast, debt funds are a type of mutual funds that invest in a myriad of debt instruments such as bonds, debentures, and money-market instruments such as treasury bills, certificates of deposit, commercial papers, etc. Each investment across any of these instruments buys you a unit. The performance of underlying securities dictates the unit price of a debt fund. These funds invest in securities with various short and long-term maturities.

Difference Between FD and Debt Funds

Choosing the right option depends on knowing the difference between FD and debt funds based on various factors. Let’s know the differences.

Return and Risk

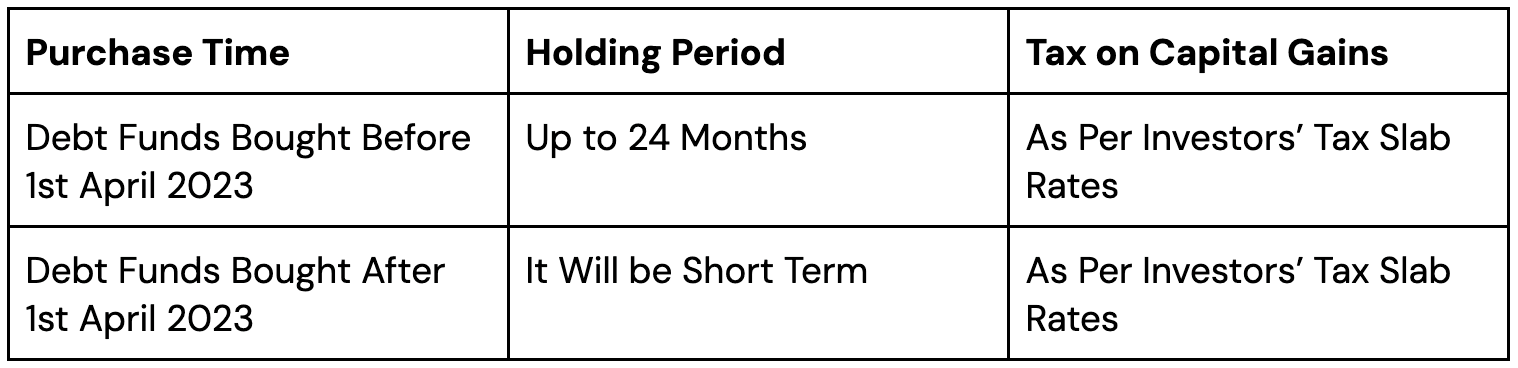

Fixed deposits offer assured returns to investors regardless of market fluctuations. The return rate is based on the investment amount and tenure. Usually, return rates remain higher for a period ranging from 1-5 years. There’s virtually no risk when investing in bank fixed deposits.

On the other hand, debt mutual funds can offer slightly higher returns than fixed deposits. But for that to happen, the underlying securities need to constantly move upward, which may not be the case throughout. So, there will always be a degree of risk involved, maybe not as high as an equity mutual fund. Debt funds allocating assets predominantly in securities with long maturities pose greater interest rate risks compared to those with short maturities.

Liquidity

You can liquidate both debt mutual funds and regular fixed deposits anytime. However, if you have invested in a close-ended debt fund or a tax-saving fixed deposit, you will need to wait for some time. A close-ended fund allows redemption only after a specified period as mentioned on the mutual fund prospectus, whereas a tax saver FD plan allows withdrawal only after five years.

Charges on Premature Withdrawal

Withdrawing before the maturity period invites exit loads in debt funds, whereas an interest penalty of 0.5%-1% is levied in the case of premature fixed deposit withdrawals. However, do note that not all debt funds will have an exit load. The percentage of exit load on a debt fund can be around 0.5%-1% depending on the asset management company’s norms. The asset management company (AMC) is the one that offers mutual funds to investors.

Application of Premature Withdrawal Charges

Exit loads are charged as a percentage of the Net Asset Value (NAV) of the debt fund units you redeem before maturity. The NAV is called the price of the debt mutual fund you have. It is calculated daily based on the performance of the underlying debt instruments. The exit load charge is levied on the NAV of the redeemed units.

An example below will help clarify.

Example - You invested INR 50,000 in a debt fund at an NAV of INR 150 in July 2024. The number of units purchased was 333.33 (50,000/150). The AMC levies an exit load of 1% for redeeming units before a year. So, if you wish to redeem your debt fund units in Feb 2025, the 1% charge will apply. Assume the present NAV is INR 140. How much an exit load will you have to pay?

Exit Load Calculation = 1% of units purchased x present NAV

= 1% of 333.33 x 140

= INR 466.67

Present Value Before Exit Load = 333.33 x 140 = INR 46,666.20

Present Value After Exit Load = 46,666.20-466.67 = INR 46,199.53

Let’s calculate the sum fixed deposit investors will get on withdrawing funds before maturity.

Here also, we can explain this with an example.

Example - You booked a fixed deposit worth INR 50,000 for three years at an interest rate of 9% per annum. After two years, you had to withdraw the sum. So, how much will you get after a penalty of, say, 1%?

Well, in premature FD withdrawals, the interest penalty applies. While some banks apply a penalty over the interest rate applicable for the time the deposit stays with them, others find the lower of the interest rate for the time it stayed with them and the contracted rate i.e. 9% in this case.

Let’s assume the bank follows the latter method to arrive at the interest penalty charge. Further, let’s assume that the interest rate for which the deposit has stayed with the bank i.e. 2 years is 7.50% per annum.

Now, the lower rate is 7.50%. The bank will deduct 1% from 7.50% to calculate your premature withdrawal sum. So, the premature FD withdrawal calculation will be made at 6.50%. The calculation says that you will get INR 56,881.95 on premature withdrawal.

While in both debt funds and fixed deposits, the eventual proceeds see a reduction. However, what needs to be noted is that in a fixed deposit, your principal amount is intact regardless of the market scenario. At the same time, you earn some interest.

On the contrary, with a debt fund, it is not certain that the investment amount is assured. With an exit load, the redemption proceeds are reduced further. Your proceeds depend on how the market performs; it may go high or low.

Taxation

This is a critical factor when comparing an FD vs Debt Fund. After all, your in-hand earnings matter!

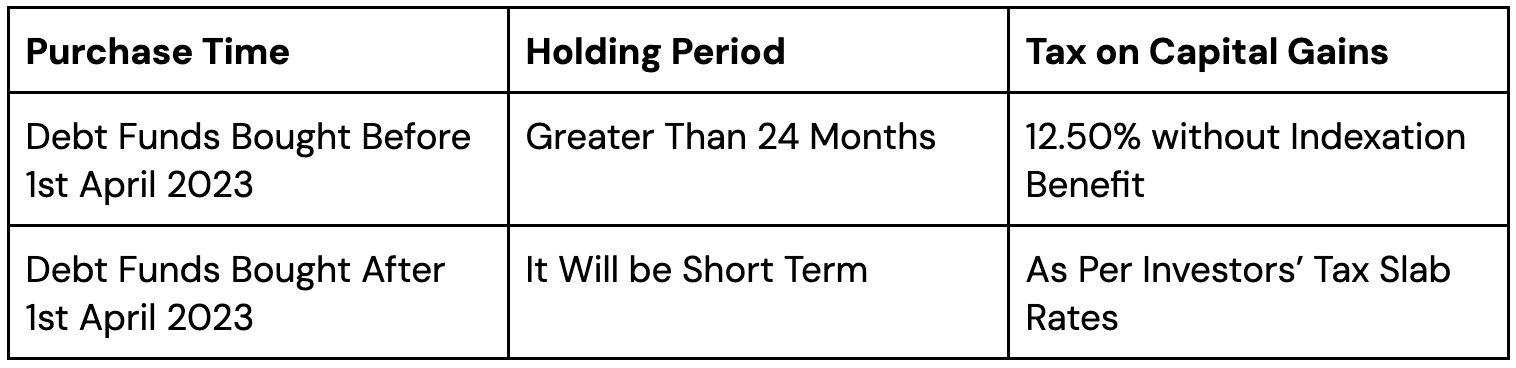

Post Budget 2024 and Budget 2025 announcements, things have changed drastically for debt mutual fund investors.

After Budget 2024, this is how debt fund gains are taxed.

Short-term Capital Gain

Long-term Capital Gain

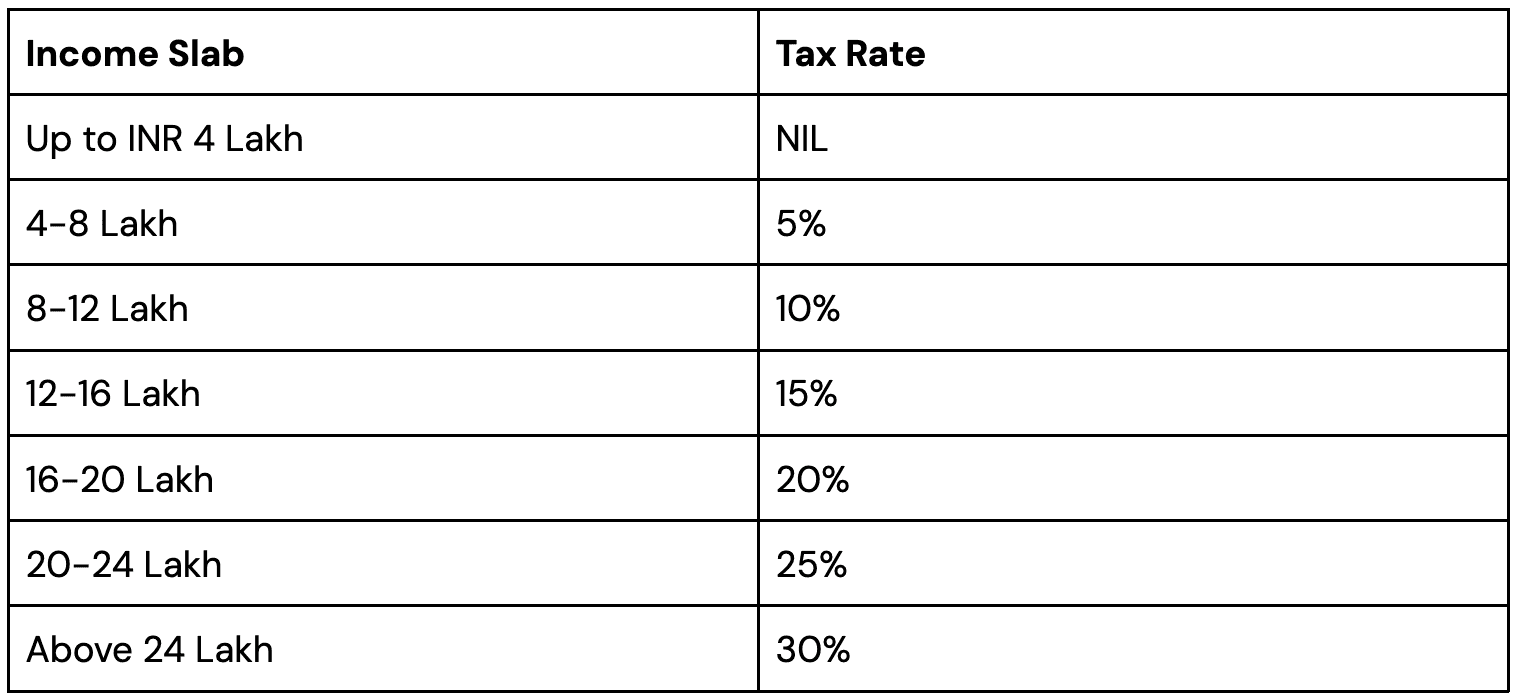

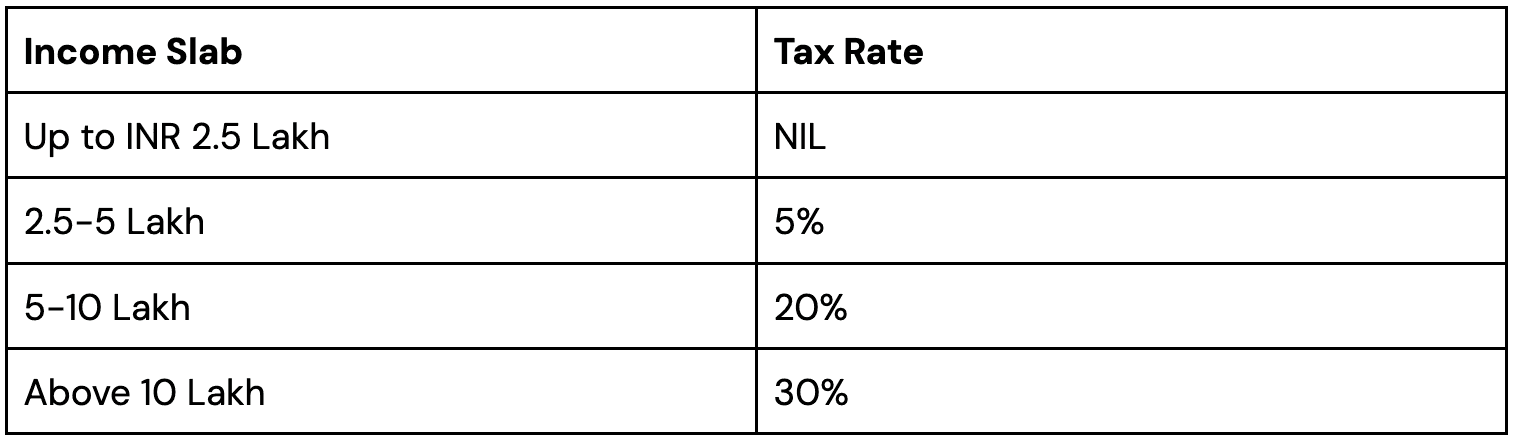

New Income Tax Slab Rates

New Tax Regime

Old Tax Regime

Indexation Benefit and How it Was Bringing Down the Tax Liability for Debt Fund Investors

The indexation benefit investors used to have before no longer exists for them after the Budget 2024 speech. This benefit was applicable to long-term capital gains i.e. profits on selling debt fund units after three years of holding them.

With indexation, redemption prices were adjusted as per the inflation, helping investors reduce their taxable income. In some cases, there were no gains as per the indexation benefit, relieving investors from the tax liability.

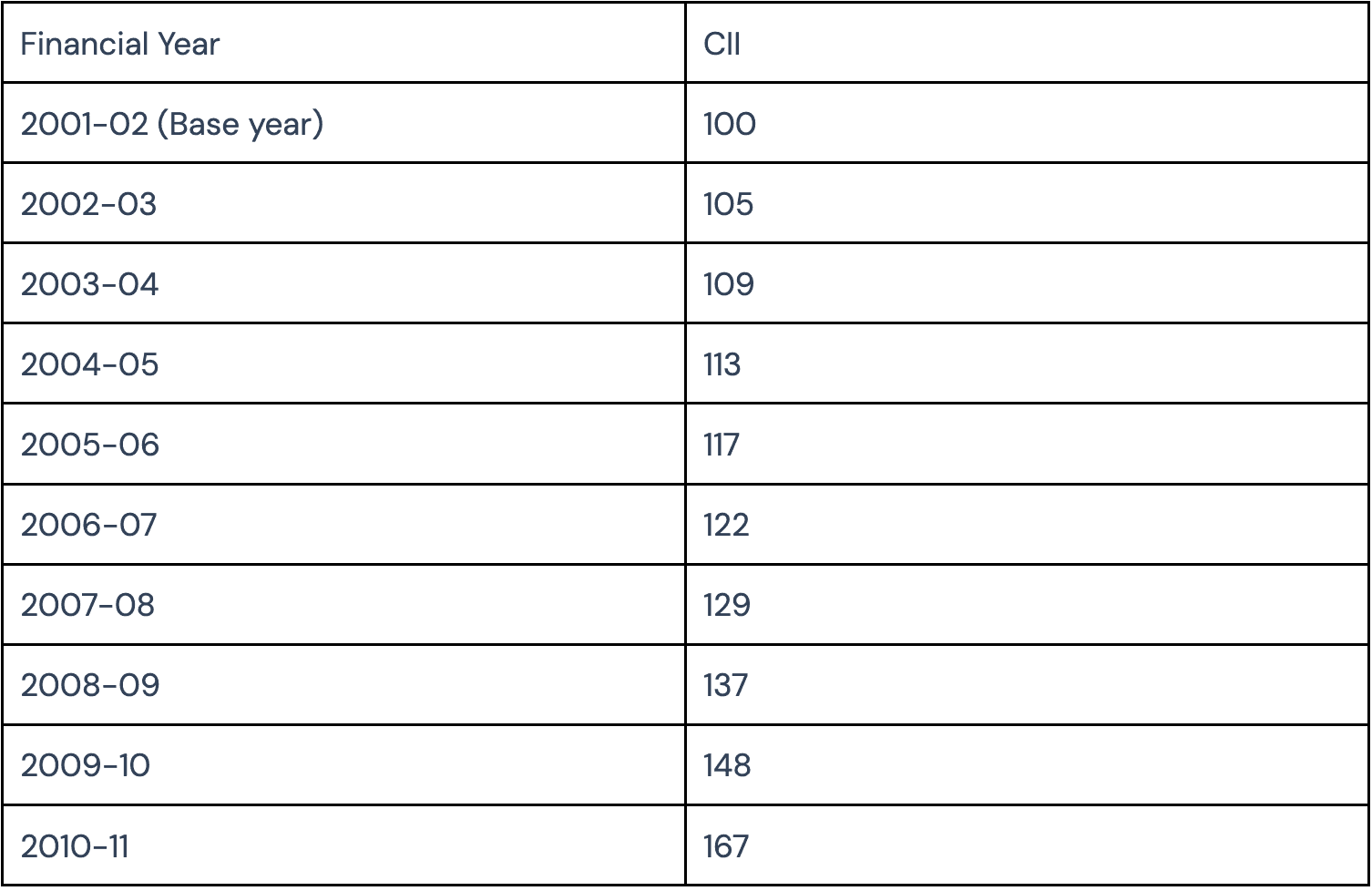

The government has a Cost Inflation Index (CII) for every financial year. The below table contains the data from FY 2001-02 to FY 2024-25 based on which taxes were calculated.

Let’s take an example to understand the impact of the indexation benefit.

Example - You invested INR 1 lakh in a debt mutual fund in June 2020 at an NAV of INR 70, which meant a purchase of 1,428.58 units. In August 2023, you sold all the purchased units at an NAV of INR 85. The selling price would have been INR 1,21,429.30, which meant a gain of INR 21,429.30. Now the proceeds must have been adjusted as per the indexed cost of acquisition derived using the following formula.

Indexed Cost of Acquisition = Original Purchase Price x (CII of the Year of Sale/CII of the Year of Purchase)

= 1,00,000 x (348/301)

= 1,15,614.61

Inflation-adjusted Income = Selling Price - Indexed Cost of Acquisition

= 1,21,429.30 - 1,15,614.61

= INR 5,814.69

20% tax would have been applied to INR 5,814.69. The tax amount would have become INR 1,162.94. The eventual amount you would have after tax is INR 1,20,266.36.

Taxation on Fixed Deposits

Taxes apply on fixed deposits as soon as the interest crosses INR 40,000 in a financial year for general citizens. For senior citizens, the threshold is raised from INR 50,000 to INR 1 lakh in the recent Union Budget 2025. The rule will, however, come into effect from April 1, 2025, onward.

Banks apply a TDS of 10% once the interest earnings cross the threshold. However, if your total earnings are up to INR 5 lakh (if you are in the old tax regime) and INR 12 lakh (if you are in the new tax regime), you can submit Form 15G/H to the bank to get the TDS waived off.

Also, there’s a tax saver fixed deposit wherein investments of up to INR 1.5 lakh in a financial year qualify for tax deductions. However, this benefit applies to investors in the old tax regime. Moreover, you can’t withdraw from it before five years.

Loan Availability

As an investor, you can get a loan against any of the two - fixed deposit or debt mutual fund. With a fixed deposit, you can get a loan/overdraft of up to 90% of the fixed deposit value. With a debt fund, the quantum of loan/overdraft is reduced to up to 70-80% of the fixed deposit value.

Which Option is Right for You?

Debt funds may offer slightly greater returns than fixed deposits. However, investment risks prevail in debt funds. If market fluctuations don’t bother you as an investor, you can invest in debt funds. However, if you are averse to market risks, stay invested in a fixed deposit. In fact, regardless of the market conditions, you should anyway keep something in a fixed deposit. The calmness it ensures while the market goes up and down is commendable.