Posted on Jan 1, 2025

Vikas Chandra Das

Financial Content Expert & Brand Storyteller

Corporate FDs vs Bank FDs - Here are the Key Differences

Trust is what matters in life. But is trusting easy, particularly when parking your hard-earned money in a fixed deposit? Not at all! A lot of things go into consideration. Like where am I putting money? Am I doing so in a bank or a Non-banking Finance Company (NBFC)? Which of the two is safe? Which yields you more? Which is more suited to my financial goals? And many more considerations like these weigh your thinking, and it’s important!

So here we’re discussing Corporate Fixed Deposit vs Bank Fixed Deposit and figuring out which you should choose to fulfil your financial goals. It’s important to weigh options carefully before deciding to invest.

What are Fixed Deposits?

Fixed deposits, technically, are a gateway to building wealth non-stop regardless of what’s going on in the market. Whether the market is skyrocketing or hitting rock bottom, your money travels the safe path with a fixed deposit. With fixed deposits in your investment portfolio, you can weather the market’s ups and downs with confidence. Around 95% of Indian households prefer investing in fixed deposits. Hands down, fixed deposits are a must!

What’s more, you have two options - banks and non-banking financial companies - from where you can book a fixed deposit. With options, comes the comparison you need to do to make the right choice. Let’s first discuss each of these separately before comparing.

What are Bank FDs?

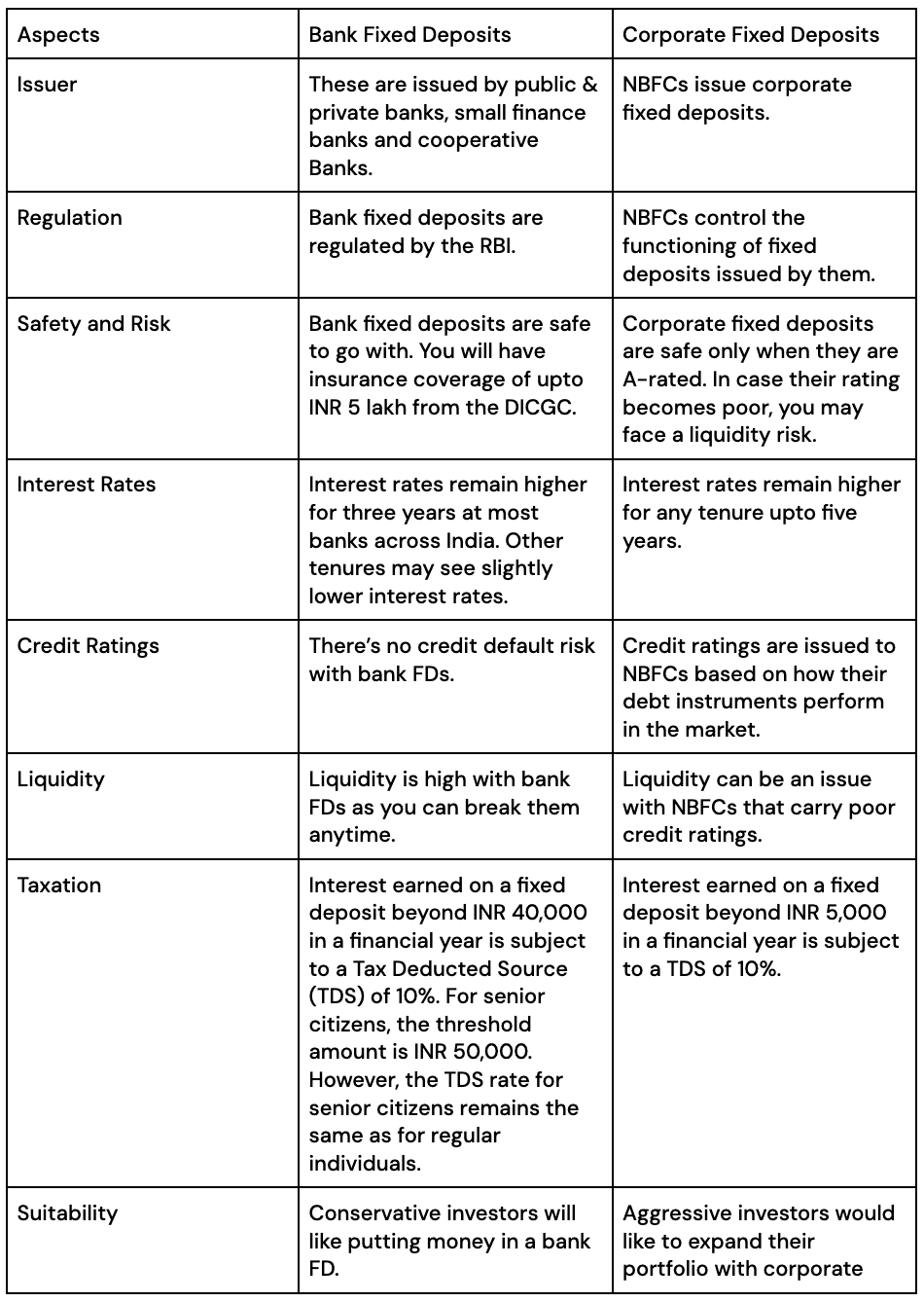

Bank fixed deposits are a type of financial instrument issued by banks for a specified period at a specified interest rate. The period can range from seven days to 10 years. The best part is that banks allow fixed deposits for odd periods such as 772 days too, instead of conventional 500 or 700 days only. It shows how flexible bank fixed deposits are for investors.

You also have cumulative and non-cumulative fixed deposit options to choose from. Both are good and serve different investment needs. While a cumulative fixed deposit lets your investments compound at an interest rate of upto 9.30% per annum, a non-cumulative fixed deposit allows you to receive periodic interest payouts to serve your regular income generation needs. What’s more, you can break your FD investments anytime, adding to the flexibility one seeks when investing in a financial instrument.

Above all, bank deposits are governed by RBI’s rules and regulations. Deposits of upto INR 5 lakh are safe under any circumstances. The RBI-owned Deposit Insurance and Credit Guarantee Corporation (DICGC) insures the same. It’s a huge comfort factor as an investor. Who would like to chase banks for fixed deposit withdrawals should they become insolvent or face other adverse circumstances? The assurance from DICGC is certainly a mood-lifter.

What are Corporate Fixed Deposits?

Corporate fixed deposits, on the other hand, are issued by non-banking financial companies (NBFCs) for tenures ranging from 12-60 months. These companies offer higher interest rates on fixed deposits. But since their fixed deposits are not insured by the DICGC cover, you as an investor should check their credit ratings assigned by Moody’s, Fitch, India Ratings and Research, ICRA, Standard & Poor’s, etc. Credit ratings range from AAA to D. While AAA, AA and A denote solid ratings, ratings after that are not considered good/ideal for investors. A-rated NBFCs are considered to have sufficient liquidity to pay back their investors compared to those with inferior ratings. So, there’s this due diligence you need to do when going for a corporate fixed deposit.

Key Differences Between Bank FDs and Corporate FDs

Let’s quickly analyse the differences between corporate FD versus bank FD on several aspects concerning a fixed deposit.

Factors to Consider When Choosing Between Corporate FDs and Bank FDs

When choosing between corporate FDs vs bank FDs, one must weigh several factors shown below.

Risk Appetite

If you are a conservative investor and want the flexibility of liquidating your investments anytime, bank FDs are made for you! Whereas if your risk appetite is higher, you can contemplate investing in a corporate fixed deposit for higher returns.

Tenure

While bank fixed deposits stay for as short as seven days and last as long as 10 years, corporate fixed deposits can be for a maximum of five years. So, if you wish to stay invested for a long time, trust bank FDs that allow you the same.

Tax Implications

Tax implications remain different for bank FDs and corporate FDs.

Interest exceeding INR 40,000 on a bank FD in a financial year will attract a 10% TDS for regular customers. Senior citizens, on the other hand, will need to pay the TDS at the same rate when the interest earned exceeds INR 50,000 in a financial year. Investors failing to submit the PAN will have to deal with a 20% TDS. If your total income falls below the taxable limit, you can avoid TDS by submitting Form 15G and Form 15H to the bank.

The threshold for corporate fixed deposits is far lower. As soon as the interest crosses INR 5,000 in a financial year, TDS at 10% will apply. Form 15G and Form 15H may not apply to corporate fixed deposits.

BharatFD - A Trusted Partner for Investing in a Fixed Deposit

BharatFD is an online platform where banks with the best FD interest rates are waiting for you. Here are some reasons that call for investing in a fixed deposit through this innovative platform.

It allows you to compare bank FDs in terms of interest rates, minimum and maximum investment limits, and several other details.

Compounds your wealth at interest rates of upto 9.30% per annum.

Communications from both banks and BharatFD upon the successful opening of a fixed deposit account.

Auto Renewal option is allowed.

FD liquidation facility is available.

Conclusion

Bank FDs and corporate FDs have their respective advantages and limitations. So, it boils down to which of the two can help you achieve your financial goals no matter what. As far as assurance of investment amount and subsequent returns are concerned, a bank fixed deposit is better. Even if we consider tax savings and the luxury of investing for a long time, bank FDs stand atop. However, if after investing in a bank FD, you have some spare amount, you can invest it in an A-rated corporate FD to maximise your gains.

Reference

What Are the TDS Rules for Fixed Deposit Interest in India? | Business Upturn