Posted on Jan 30, 2025

Vikas Chandra Das

Financial Content Expert & Brand Storyteller

Fixed Deposits for NRIs: A Guide to Non-Resident Fixed Deposits

Are you a non-resident Indian (NRI) looking to earn attractive interest by opening a fixed deposit account in India? You’ve got multiple options to choose from. There are many banks with attractive NRI fixed deposit schemes. Some of these deposits also remain tax-free on the interest earned. It’s a win-win situation for you! However, you may need a complete guide to investing in NRI fixed deposits to make an informed decision. We understand that and have thus presented the details concerning NRI fixed deposits in India below.

What Do You Mean by NRI Fixed Deposits?

Fixed deposits are a way for NRIs to earn over their surplus income. No matter where they have earned income, whether in India or abroad, NRIs can park that in a fixed deposit to grow it further. They can deposit a specific amount for a specific period to make it bigger courtesy of impressive fixed deposit interest rates. These deposits offer NRIs guaranteed income and let you add a joint holder and an overdraft facility to meet your instant financial needs.

Eligibility Criteria for Opening an NRI Fixed Deposit Account in India

A Non-resident Individual, Person of Indian Origin (PIO) or Overseas Citizen of India can open a NRI fixed deposit in India. All you need to do is check the tenure and amount that yields you the highest fixed deposit interest rates. Once done, you can go ahead and book an FD.

Types of NRI Fixed Deposits

The prevailing Foreign Exchange Management Act (FEMA) regulations state that NRIs can open the following fixed deposit accounts in India.

Non-resident External (NRE) Deposit

Non-resident Ordinary (NRO) Deposit

Foreign Currency Non-resident (FCNR) Bank Deposit

NRE Fixed Deposit Account

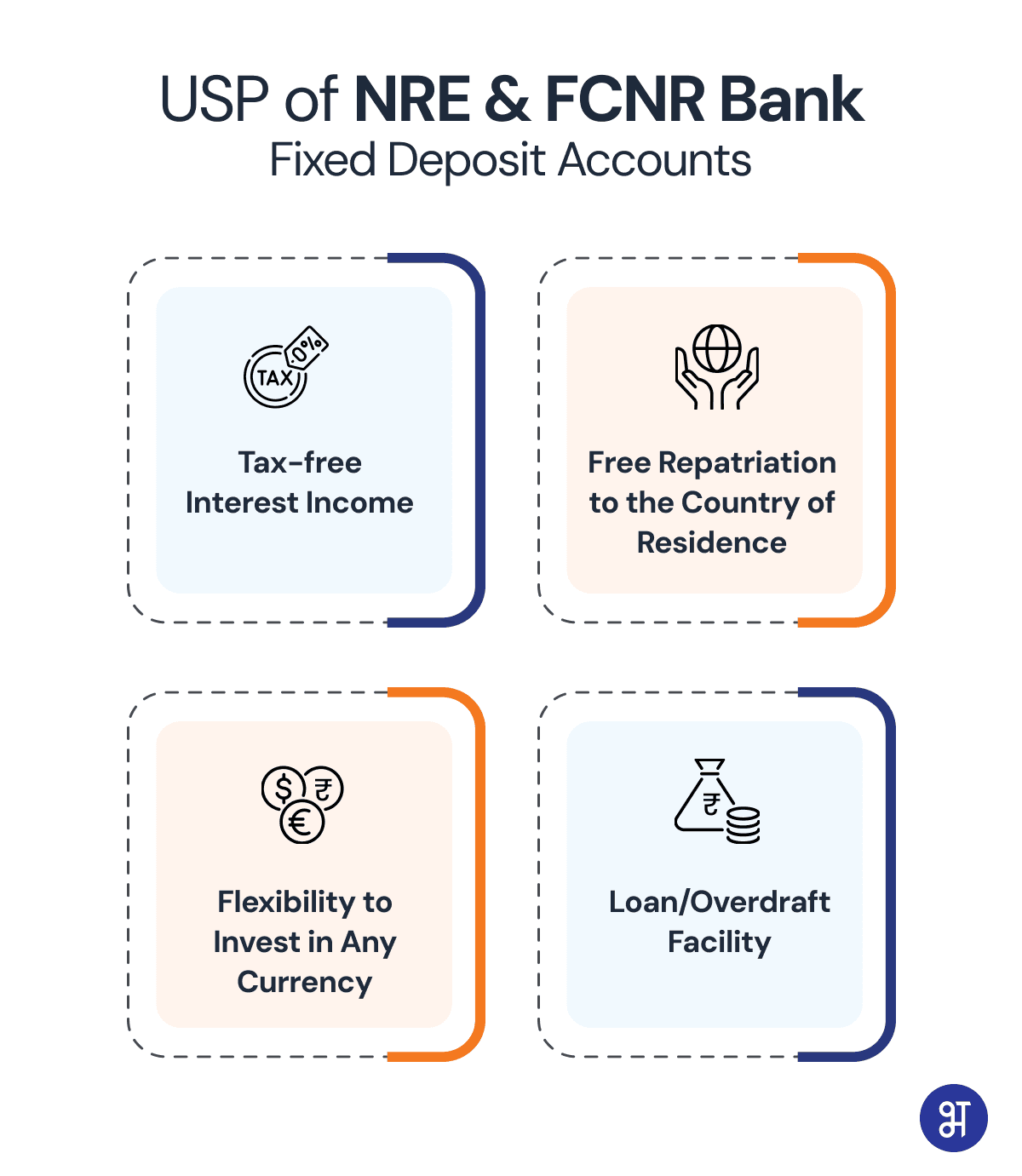

As an NRI, if you want to grow your overseas earnings, consider opening an NRE fixed deposit account in India. The interest earned on the same is tax-free and is fully repatriable along with the investment amount.

NRO Fixed Deposit Account

This fixed deposit is designed for those NRIs who earn in India through rent, pensions, investments and other legal sources. The repatriation is allowed for up to US$ 1 million for all the NRO fixed accounts an NRI opens in India. However, the interest earned on NRO fixed deposits is subject to taxation as per the prevailing rules.

FCNR Bank Fixed Deposit Account

This fixed deposit is a product by which NRIs can open a fixed deposit in a foreign currency to stay protected against currency fluctuations. The foreign currencies allowed for this fixed deposit are the US Dollar, Canadian Dollar, Australian Dollar, British Pound, Japanese Yen and Euro. NRIs can get their funds repatriated fully with this account.

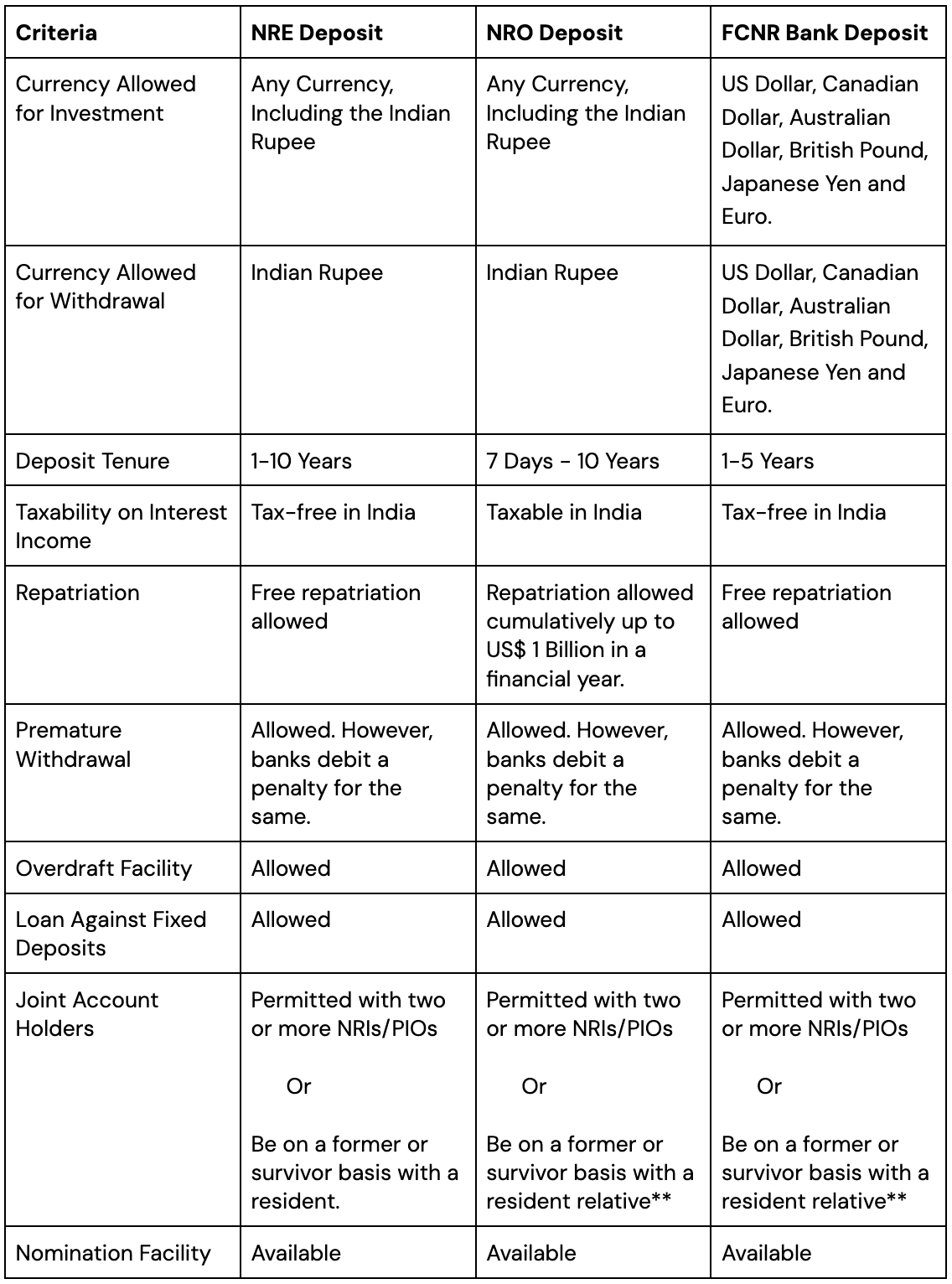

Parameters for Different NRI Fixed Deposits in India

Figuring out the differences between NRI fixed deposit accounts in India becomes simple with the below table. Check it out!

Key Benefits of NRI Fixed Deposits

High Interest Rates

NRI fixed deposits can earn you interest at as high as 8% per annum across banks in India. The high rates will help raise your earnings substantially.

Tax-Free Options

Earnings when free of taxes delight investors further. NRE and FCNR Bank fixed deposits come with tax-free interest income for NRI investors.

Repatriation

As an NRI investor, you would want all your funds repatriated to the country of your residence. To your delight, both NRE and FCNR Bank fixed deposits allow you free repatriation. Whereas NRO deposits allow you to repatriate up to US$ 1 billion each financial year.

Loan and Overdraft Facilities

NRI investors can get both loan and overdraft facilities against fixed deposits to meet their liquidity needs. Their fixed deposits will act as collateral for these credit facilities. The interest rates will thus be lower compared to when taking unsecured loans.

Nomination Facility

NRI fixed deposits also feature a nomination facility by which investors can nominate their family members. So, if they die during the fixed deposit term, the proceeds will be transferred to their dear ones. It’s a shield for uncertain times we usually don’t account for.

Auto-renewal Option

You can even use the auto-renewal option on your NRI fixed deposits in India to continue receiving benefits without any breaks.

Tax Implications

NRE and FCNR Bank fixed deposits come up with zero tax on interest earnings for investors. NRO deposits, on the other hand, are subject to a tax deducted at source (TDS) of 30% along with applicable surcharge and fees. According to Section 206AA introduced by Finance (No. 2) Act, 2009, every NRI who will have TDS deductible on interest income need to submit PAN to the deductor. In case of non-adherence to this rule, the TDS will be the higher of the maximum marginal rate or 30% along with applicable surcharge and fees.

However, there is a Double Taxation Avoidance Agreement (DTAA) by which NRIs can avoid being taxed in two countries - the country where they earn and the country where they are a tax resident. India has signed DTAA with over 90 countries, including Australia, the USA, the UK, Germany, France, Canada, Singapore, Portugal and Hong Kong.

Opening an NRI Fixed Deposit Account

Online Process - You can book an NRE fixed deposit account using the mobile banking app or Internet banking.

Offline Process - Visit the nearest branch of the bank with whom you wish to open a NRI fixed deposit account.

Documentation Required for NRIs

Form 60 or PAN Card

Valid Passport

NRI Status (Employment/Residence Permit/Residence Visa or Work)

Indian and Overseas Address Proofs

Recent Passport Size Photograph

Documentation Required for PIOs

Form 60 or PAN Card

Valid Passport

PIO Status (Valid OCI or PIO Card)

Indian and Overseas Address Proofs

Recent Passport Size Photograph

A Signed and Filled PIO Declaration Form

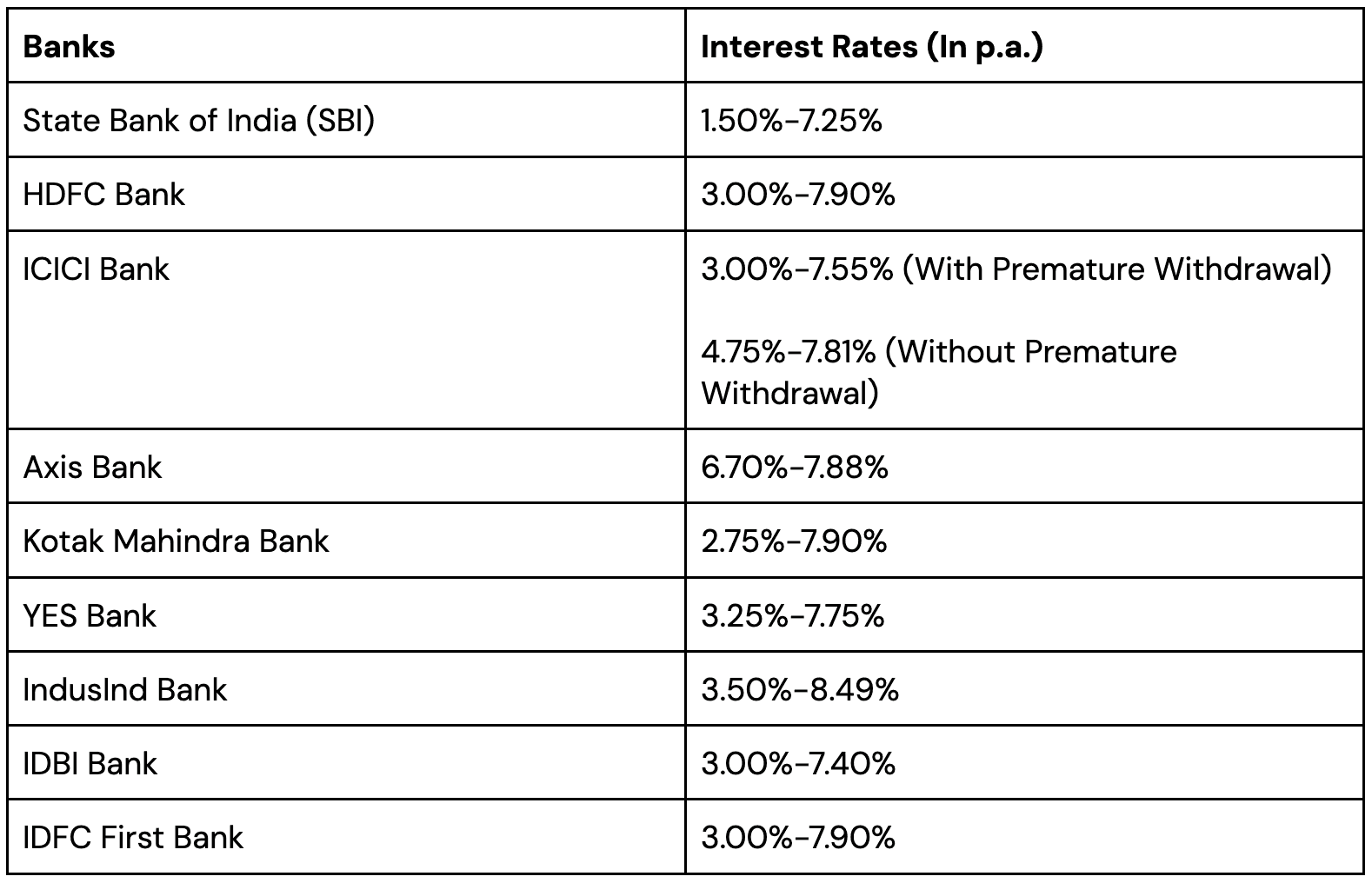

NRI Fixed Deposit Rates in India

Final Words

NRI fixed deposits certainly have numerous advantages. They offer the flexibility to invest in numerous foreign currencies, a loan facility against a fixed deposit, besides being a tax-free alternative for NRE and FCNR Bank deposit investors. Do weigh your options carefully before opening a NRE fixed deposit account in India.

Frequently Asked Questions (FAQs)

What is an NRI Fixed Deposit?

An NRI fixed deposit is a type of term deposit that helps Non-resident Indians to invest their surplus income and earn high interest on it.

What are the Different Types of NRI Fixed Deposits?

There are three types of NRI Fixed Deposits in India - NRE, NRO and FCNR Bank Deposit accounts. With an NRE deposit, NRIs can invest foreign earnings in the Indian currency and get them fully repatriated freely to their country of residence. The interest earned is tax-free. NRO accounts allow deposits from NRIs having earned in India through rent, pensions and other income. FCNR Bank Deposit allows NRIs to invest in foreign currencies, earn tax-free interest and have their funds repatriated freely to their country of residence.

What is the eligibility to open an NRI FD?

NRIs, Overseas Citizens of India and Persons of Indian Origin are eligible to open an NRI FD account.

Are NRI Fixed Deposits tax-free?

The interest earned on NRE and FCNR Bank deposits remains tax-free. However, the interest earned on NRO deposits is subject to a 30% TDS along with surcharge and cess. However, with a Double Taxation Avoidance Agreement (DTAA), depositors can reduce their tax liability.

Can I take a loan against my NRI FD?

Yes, NRIs can take a loan or overdraft facility against fixed deposits.

What is the minimum tenure for NRI FDs?

NRI FDs can have a minimum tenure of seven days, depending on the bank’s norms.

How do I choose the right NRI FD for me?

Consider choosing the bank that offers high interest rates and allows you to invest in different currencies. Besides, do consider taxability before choosing the right NRI FD.